Claim Automation AI: Insurance with Smarter Claim Processing AI

- March 13

- 29 min

AI-based underwriting in insurance refers to the use of artificial intelligence technologies, such as machine learning and generative AI, to automate and enhance the underwriting process. It enables insurers to analyze vast datasets, improve risk assessment accuracy, and streamline workflows, resulting in faster, more precise underwriting decisions. By integrating AI-driven underwriting, insurers can offer competitive pricing, detect fraud, and provide a better customer experience while optimizing operational efficiency.

Artificial intelligence is rapidly reshaping the landscape of insurance underwriting, moving the industry from manual, legacy processes to dynamic, AI-driven operations. By integrating generative AI and machine learning, insurers can streamline workflows, enhance risk accuracy, and offer competitive pricing that meets modern consumer demands.

This article explores how AI in insurance underwriting is revolutionizing risk assessment, offering practical use cases, highlighting key benefits, and addressing the challenges of implementation. Read on to learn how AI for underwriting is transforming the insurance business and what it means for the future of underwriting technology.

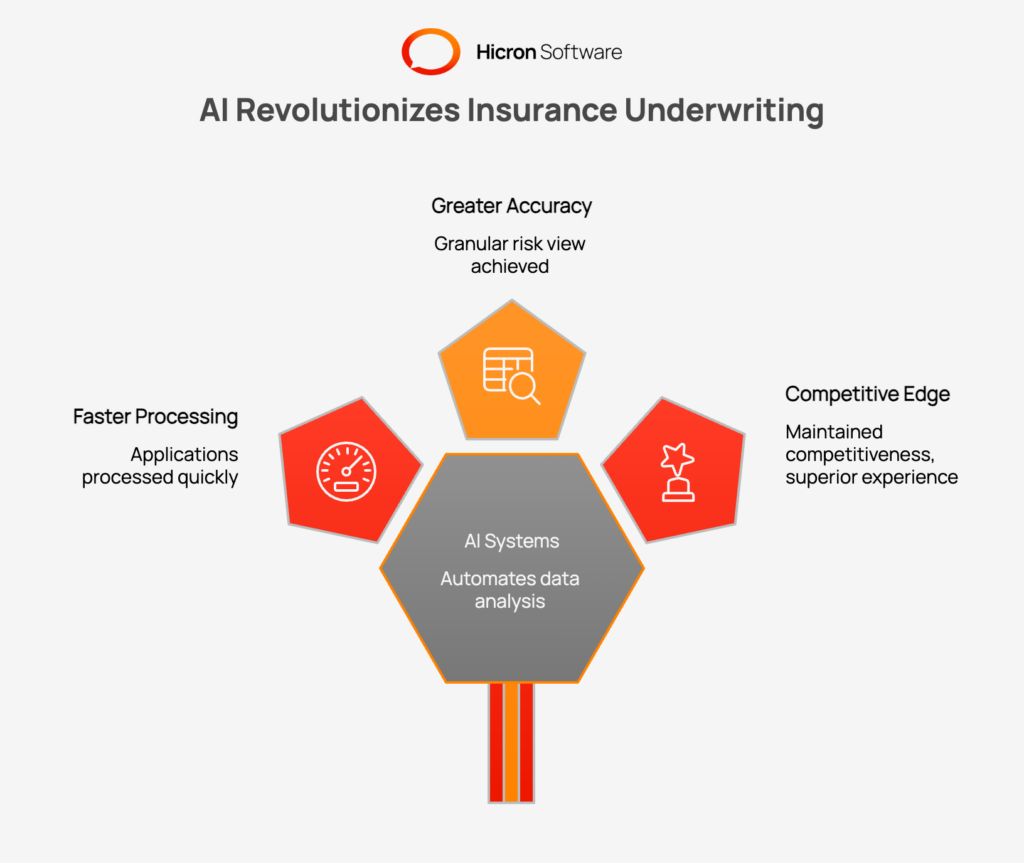

The traditional underwriting process has long been the backbone of the insurance industry, relying heavily on historical data, manual forms, and human intuition to assess risk. While effective in the past, existing underwriting methods often face limitations in speed and precision, leading to delays and potential inconsistencies in underwriting decisions. Today, AI is improving underwriting by automating data analysis and introducing predictive capabilities that were previously impossible. AI enables insurers to process applications faster and with greater accuracy, fundamentally shifting how risk is evaluated.

This revolution is about precision. AI underwriting systems in insurance enable the ingestion of vast amounts of structured and unstructured data, providing a granular view of risk that human underwriters alone cannot achieve. As competition heats up, the use of AI has become a critical differentiator. Insurance companies that embrace AI solutions are better positioned to maintain competitiveness, offer superior customer experiences, and manage their loss ratios effectively.

Risk assessment is the core function of insurance underwriting. It is the mechanism by which an insurer determines the likelihood of a claim and sets the premium accordingly. Underwriting is crucial because it directly impacts the insurer’s profitability and solvency. If an insurer underestimates risk, they face financial losses; if they overestimate it, they lose customers to competitors. Accurate risk profiling is therefore essential for sustainable business operations.

Underwriting technology has evolved to support this critical task, but the complexity of modern risks, from cyber threats to climate change, demands more sophisticated tools. AI enables insurers to refine their risk assessment capabilities, moving beyond broad generalizations to individual risk profiles. This precision ensures that insurance policies are priced fairly and competitively, securing the financial health of the insurer while meeting the specific needs of the policyholder.

AI enhances insurance risk assessment by analyzing vast, complex datasets in real-time, identifying patterns and correlations that human underwriters might miss. It improves predictive modeling, enabling insurers to forecast risks with greater accuracy and adapt to emerging threats like cybersecurity or climate change. This leads to more precise risk profiles, competitive pricing, and proactive risk management.

One of the advantages of AI is its ability to process massive datasets that would overwhelm human analysts. AI enables insurers to process diverse data sources, from traditional policyholder records and demographic data to external risk factors like geospatial information or social media sentiment. Machine learning algorithms can sift through this information in seconds, identifying relevant risk indicators that might otherwise be buried in mountains of paperwork.

For example, when assessing property insurance risks, AI can analyze satellite imagery, local weather patterns, and crime statistics simultaneously. Integrating these data points allows for a comprehensive view of the risk landscape. By utilizing real-time data feeds, AI-based underwriting helps insurance companies maintain continuously updated risk profiles, ensuring that the insurer’s underwriting decision is based on the most current information available rather than outdated historical snapshots.

AI models excel at pattern recognition, detecting subtle correlations across vast datasets that human underwriters might miss. This capability is vital for accurate risk scoring. AI can analyze years of claims data to identify specific behaviors or conditions that precede a loss. By recognizing these patterns, AI aids in predicting customer behavior, such as the likelihood of filing claims or letting a policy lapse.

For instance, in life insurance, AI can analyze combinations of lifestyle factors, medical history, and even purchasing habits to predict longevity and health risks with remarkable accuracy. These insights allow insurers to assign more precise risk scores. AI can handle the complexity of multivariate analysis, ensuring that the underwriting process reflects a holistic understanding of the applicant’s risk profile rather than relying on a few binary factors.

Predictive modeling is a powerful use case for AI in underwriting. By leveraging advanced analytics, insurers can forecast future risks with a higher degree of confidence. AI models are particularly effective at modeling emerging risks that lack extensive historical data, such as those related to climate change or cybersecurity threats. These models can simulate various scenarios to predict potential losses, allowing insurers to adjust their underwriting strategies proactively.

For example, AI helps insurers anticipate the impact of rising sea levels on coastal properties or the likelihood of a data breach based on a company’s cybersecurity posture. This enhances the overall accuracy of the risk assessment, enabling the insurer to avoid bad risks and capitalize on good ones. The power of AI lies in its ability to constantly learn and adapt, meaning these predictive models become more accurate over time as they ingest more data.

Precision is key to profitability in the insurance business. AI facilitates the creation of highly detailed risk profiles, which directly links to more accurate policy pricing. Instead of placing customers into broad risk pools, insurers use AI to tailor premiums to the specific risk level of the individual or business. This allows for more competitive pricing for low-risk customers, effectively attracting and retaining the most desirable business.

This granular approach helps insurers balance competitiveness with profitability. By avoiding underpricing high-risk policies and overpricing low-risk ones, the insurer optimizes its portfolio. AI enables insurers to process these calculations instantly, providing quotes that are both attractive to the customer and financially sound for the company. This level of pricing sophistication is reshaping insurance underwriting strategies across the market.

The most immediate benefit of AI in underwriting is the dramatic increase in speed and efficiency. Traditional underwriting workflows often involve manual data entry, back-and-forth communication, and lengthy review periods. AI automates many of these routine underwriting tasks, reducing the time needed to assess risk and approve policies from days or weeks to minutes or even seconds.

This efficiency enables insurers to process higher application volumes without causing delays or requiring additional headcount. Streamlining the process means that the average underwriting decision happens much faster, which is crucial in today’s instant-gratification economy. By removing bottlenecks, AI enables insurers to capture revenue faster and improve operational throughput.

Beyond assessing risk, AI is a powerful tool for risk mitigation and fraud detection. AI systems can spot anomalies in application data that may indicate fraudulent activity. For example, AI helps flagging unusual patterns, such as inconsistencies in reported income versus public records, or rapid-fire policy applications from the same IP address. Identifying these red flags during the underwriting process prevents bad risks from ever entering the books.

Furthermore, AI-driven insights can help policyholders mitigate their own risks. An insurer might use AI to analyze a commercial client’s operations and suggest specific safety improvements to lower their premium. This proactive risk management benefits both the insurer, by reducing claims, and the client, by lowering costs and improving safety.

Customer experience is a major battleground for insurers, and AI plays a pivotal role here. Modern consumers expect smooth, digital experiences like those they receive from tech giants. AI allows insurers to deliver personalized insurance products and pricing that align closely with individual risk profiles. When a customer receives a quote that feels tailored to their specific situation, satisfaction increases.

AI improves trust through transparency. While complex algorithms can be opaque, the speed and consistency of AI-driven decisions reduce the frustration of long waiting periods. By streamlining the application process and providing instant feedback, AI helps insurance companies build stronger relationships with their policyholders. A smooth, fast, and fair underwriting process is a key driver of customer retention.

Navigating the regulatory landscape is a constant challenge for the insurance industry. AI helps support compliance by maintaining rigorous records of data usage and decision-making parameters. Advanced analytics can be used to audit underwriting models to ensure they adhere to fair pricing standards and do not discriminate against protected classes.

Leveraging AI allows insurers to maintain data accuracy and transparency during audits. By automating the documentation of how risk assessments are derived, insurers can more easily demonstrate to bodies like the National Association of Insurance Commissioners that their practices are sound and compliant. This reduces the legal and reputational risks associated with non-compliance.

A classic use case of AI in underwriting is dynamic pricing in auto insurance. Insurers leverage telematics devices and smartphone apps to collect real-time data on driving behavior, speeding, hard braking, and time of day driven. AI analyzes this data to offer usage-based premiums.

Instead of relying solely on proxies like age or credit score, the insurer assesses risk based on actual behavior. Safe drivers are rewarded with lower rates, while risky behaviors result in higher premiums. This AI-driven approach incentivizes safer driving and aligns the price of the insurance policy directly with the risk presented.

Cyber insurance is a rapidly growing field where AI is indispensable. Underwriting cyber risk is notoriously difficult due to the constantly evolving nature of threats. AI models can scan a company’s digital footprint, assessing vulnerabilities in their infrastructure, such as unpatched software or open ports.

Based on this non-invasive scan, AI can generate a risk score and help underwriters tailor cyber insurance policies that match the specific exposures of the client. AI also enables continuous monitoring, allowing insurers to adjust coverage or alert clients if their risk profile changes due to a new vulnerability.

In the realm of life and health insurance, AI is enabling a shift towards personalized wellness. Insurers are integrating data from wearable health devices (with user consent) into the underwriting process. AI algorithms analyze trends in physical activity, heart rate, and sleep patterns to estimate overall health risks more accurately than a one-time medical exam.

This allows for the creation of personalized risk profiles that reward healthy lifestyles. It also speeds up the process; “fluid-less” underwriting (without blood or urine samples) is becoming more common as AI helps insurers rely on alternative data sources to assess mortality and morbidity risk with high confidence.

One of the major challenges is the “black box” nature of some complex AI models. Underwriters and regulators need to understand how an AI system arrives at an underwriting decision. This is where the concept of responsible AI becomes crucial. Insurers must develop transparent and explainable AI models to ensure fairness and avoid bias. The National Association of Insurance Commissioners (NAIC) and other regulatory bodies are increasingly focused on the ethical use of AI, and insurers must navigate a complex regulatory landscape.

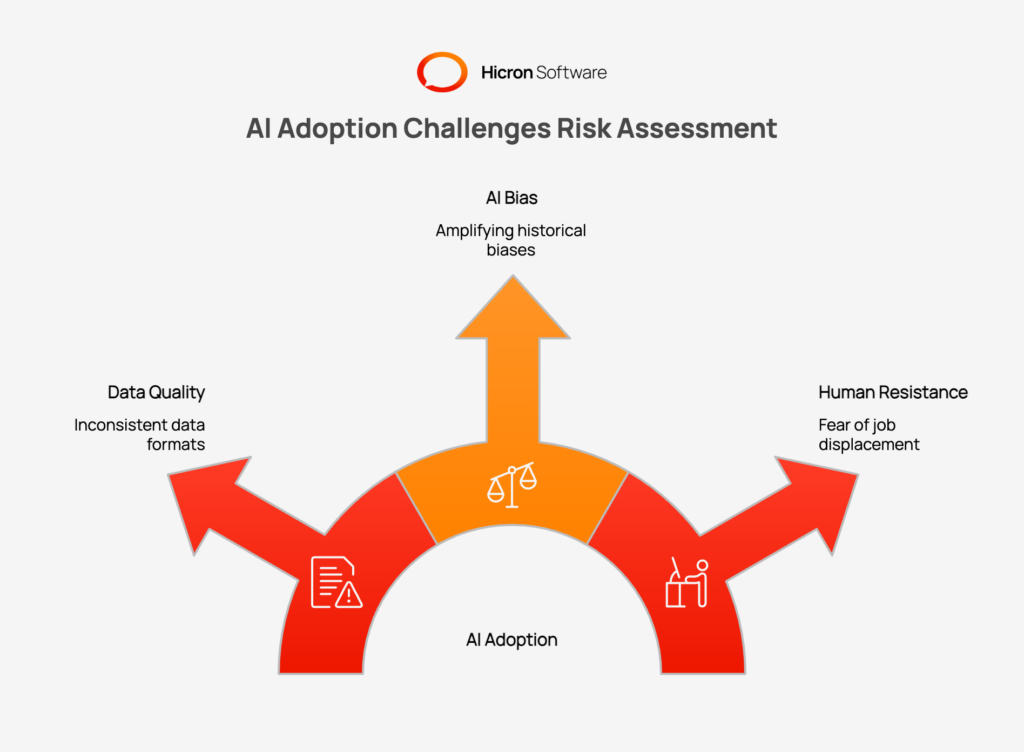

Despite the benefits, implementing AI is not without hurdles. A primary challenge is data quality. AI models are only as good as the data they are fed. Many insurers struggle with inconsistent data formats and fragmented legacy systems that trap data in silos. Merging these disparate sources into a clean, structured dataset suitable for AI analysis is a massive undertaking.

Insurers must invest heavily in data engineering to overcome these integration issues. Without a unified data architecture, deploying AI solutions effectively is nearly impossible. Ensuring data integrity is the first step toward successful AI adoption.

Another challenge is managing bias. If historical data contains biases (e.g., against certain demographics), AI models trained on that data can inadvertently perpetuate or even amplify those biases. This leads to unfair underwriting decisions and potential regulatory penalties.

Responsible AI practices are essential. Insurers must actively test their models for disparate impact and implement strategies to ensure ethical and unbiased risk assessments. This involves continuous monitoring and “human-in-the-loop” oversight to verify that the AI system is acting fairly.

There is often cultural resistance to AI adoption, particularly from underwriters who fear job displacement. However, AI cannot replace the nuance of human judgment in complex cases. The challenge lies in balancing human expertise with AI insights.

The goal should be to position AI as a tool that augments the underwriter, not replaces them. AI handles the routine, high-volume tasks, freeing up human experts to focus on complex, high-value risks that require negotiation and intuition. Building a collaborative approach where AI supports the underwriter is crucial for cultural acceptance and operational success.

To deploy AI responsibly, insurers must prioritize transparency, fairness, and accountability. This starts with building explainable AI models. An insurer must be able to articulate why an AI system made a particular recommendation, especially in cases of adverse decisions. This transparency is not only essential for regulatory compliance but also for building trust with customers and underwriters. The insurer’s underwriting team needs to have confidence in the AI tools they use daily.

Developing a strong governance framework is also a critical component of responsible AI. This framework should outline the principles for the ethical use of AI, establish processes for monitoring AI models for bias, and define clear lines of accountability.

|

Component |

Details |

|

Ethical Principles |

Define fairness, transparency, accountability, and non-discrimination as guiding principles; use AI to augment human decision-making, not replace it. |

|

Bias Monitoring and Mitigation |

Regularly test AI models for bias to ensure equitable outcomes; train with diverse, representative datasets to minimize skewed results. |

|

Accountability and Oversight |

Set clear roles and responsibilities for monitoring AI performance; establish an AI ethics committee for compliance with ethical guidelines, AI use cases, and regulations. |

|

Regular Audits and Updates |

Perform periodic audits of AI systems for ethical alignment and effectiveness; update models continuously to meet new data, regulations, and expectations. |

|

Transparency and Communication |

Ensure AI decisions are explainable; provide clear reasoning for underwriting outcomes and communicate AI usage to all stakeholders, including customers. |

Insurers must ensure their AI systems do not perpetuate or amplify existing societal biases. Incorporating AI ethically means conducting regular audits of AI-based underwriting systems and ensuring that the technology is used to augment human intelligence, not replace it entirely. AI must be a tool that empowers underwriters to make better, fairer decisions.

The future of AI in insurance underwriting lies in real-time risk monitoring. By incorporating IoT devices and live data streams, insurers can move from static, one-time risk assessments to continuous underwriting. For example, smart sensors in homes can provide real-time updates on water leaks or fire hazards for property insurance.

This allows the insurer to adjust risk profiles dynamically. If a risk is detected, the insurer can alert the homeowner to fix it before a claim occurs, shifting the model from risk transfer to risk prevention.

Advanced technologies like Natural Language Processing (NLP) are expanding what AI can handle. NLP allows AI to read and understand unstructured data, such as medical notes, claims descriptions, or legal contracts. This unlocks a treasure trove of information that was previously inaccessible to automated systems.

Generative AI models for insurers can use NLP to interpret complex industry reports or summarize lengthy policy documents, enhancing risk evaluations. This allows for a deeper, more qualitative analysis of risk at scale.

As AI technology matures, we will see the total automation of routine underwriting processes. Intelligent automation tools will handle the end-to-end underwriting for standard, low-complexity risks. This allows insurers to scale their operations massively without linear cost increases.

For example, AI systems will automatically triage applications, approving low-risk ones instantly and routing complex ones to human specialists. This hybrid model ensures efficiency for the majority of cases while reserving human intellect for where it adds the most value.

1. Audit Systems and Processes for AI Readiness

2. Partner with AI Solution Providers

3. Train Underwriters on AI Tools

Successful implementation starts with an audit. Insurers must assess their current systems to identify gaps in data management and technology infrastructure. Is the data accessible? Are the current underwriting systems compatible with modern AI tools?

Ensuring AI readiness involves cleaning data, upgrading legacy platforms, and establishing clear goals for what the AI solution is expected to achieve. This foundational work is critical for a smooth deployment.

Developing AI from scratch is resource-intensive. Partnering with specialized AI solution providers can accelerate the journey. These vendors bring experience in insurance analytics and proven AI deployment strategies.

Collaborating allows insurers to create customized AI algorithms tailored for specific lines of business or risk types. It leverages external expertise to avoid common pitfalls and speed up time-to-market.

Finally, the human element cannot be ignored. Training underwriters on AI tools is essential. Teams need to understand how to interpret AI scores, how to spot potential errors in the model, and how to utilize AI insights for better decision-making.

Insurers must foster a culture of learning, helping their workforce adapt to these new technologies. When underwriters feel confident using AI, the technology becomes a powerful asset rather than a source of friction.

AI in insurance underwriting is no longer a futuristic concept; it is a present-day necessity. From analyzing vast datasets and identifying hidden patterns to automating routine tasks and enhancing customer experience, AI offers a comprehensive toolkit for smarter risk assessment. The benefits of AI underwriting, precision, speed, and efficiency, are transforming the insurance industry fundamentally.

As the market evolves, AI adoption is becoming essential for insurers to remain market leaders. Those who successfully integrate AI into their underwriting workflows will enjoy competitive pricing, better risk management, and higher profitability. Now is the time for insurers to explore the insurance underwriting process with AI solutions, leverage generative AI applications, and embrace the future of data-driven underwriting to stay ahead in an increasingly complex world. Contact us to discuss, plan and scope your AI solution further.

AI in insurance underwriting uses technologies like machine learning to automate and enhance the process of risk assessment. Its primary role is to analyze vast amounts of data quickly and accurately, allowing insurers to make faster, more precise decisions about which risks to insure and at what price. This leads to increased efficiency, better risk management, and more competitive pricing.

AI improves risk assessment by processing diverse datasets—including real-time information from sources like IoT devices and telematics—that are too complex for manual analysis. It identifies subtle patterns and predicts future risks with greater accuracy than traditional methods, which rely on historical data and broader assumptions. This enables insurers to create highly personalized risk profiles for more precise and fair policy pricing.

The main challenges include issues with data quality and integration, as AI models require clean, comprehensive data from often fragmented legacy systems. Another significant challenge is managing potential AI bias to ensure ethical and fair underwriting decisions, which requires careful model monitoring and adherence to responsible AI practices. Finally, there’s a need to manage the cultural shift by training underwriters to work effectively with new AI tools.

Hicron Software proved to be a trusted partner with unmatched technical expertise, delivering a scalable and user-friendly web application that was pivotal to our successful U.S. market expansion.

Hicron’s contributions have been vital in making our product ready for commercialization. Their commitment to excellence, innovative solutions, and flexible approach were key factors in our successful collaboration.

I wholeheartedly recommend Hicron to any organization seeking a strategic long-term partnership, reliable and skilled partner for their technological needs.

After carefully evaluating suppliers, we decided to try a new approach and start working with a near-shore software house. Cooperation with Hicron Software House was something different, and it turned out to be a great success that brought added value to our company.

With HICRON’s creative ideas and fresh perspective, we reached a new level of our core platform and achieved our business goals.

Many thanks for what you did so far; we are looking forward to more in future!

Hicron is a partner who has provided excellent software development services. Their talented software engineers have a strong focus on collaboration and quality. They have helped us in achieving our goals across our cloud platforms at a good pace, without compromising on the quality of our services. Our partnership is professional and solution-focused!

The IT system supporting the work of retail outlets is the foundation of our business. The ability to optimize and adapt it to the needs of all entities in the PSA Group is of strategic importance and we consider it a step into the future. This project is a huge challenge: not only for us in terms of organization, but also for our partners – including Hicron – in terms of adapting the system to the needs and business models of PSA. Cooperation with Hicron consultants, taking into account their competences in the field of programming and processes specific to the automotive sector, gave us many reasons to be satisfied.