Claim Automation AI: Insurance with Smarter Claim Processing AI

- March 13

- 29 min

Risk-based pricing is a methodology used by lenders and insurers to set prices and rates based on an individual assessment of a customer’s risk profile. Customizable underwriting workflows are the operational frameworks that support this, allowing organizations to automate, segment, and manually review applications according to predefined rules and risk levels.

This article provides a detailed guide for creating sophisticated underwriting systems. It explains the process of setting objectives, collecting and analyzing data, and building pricing models. You will learn how to design automated workflows that improve speed and accuracy. The content also covers the technology needed to support these processes, the importance of regulatory compliance, and the methods for testing and refining your system. This piece offers a foundational understanding for businesses looking to implement more precise and efficient risk management practices in insurance, ultimately improving profitability and customer satisfaction through tailored insurance services.

Key Takeaways:

The first step in creating a risk-based pricing structure is to define clear business goals. Before exploring data or technology, it is essential to establish what the organization intends to accomplish. These objectives provide direction for the entire project. Goals may include:

Each objective should align with the company’s broader strategic vision.

For example, if a company’s brand focuses on providing fast service, its underwriting workflows should prioritize speed and automation. If its focus is on serving a specific market niche, the risk models should be tailored to that segment’s unique characteristics. A clear set of goals ensures that every decision made during the development process supports the intended business outcomes. It also helps to align different departments, from technology to compliance, toward a common purpose.

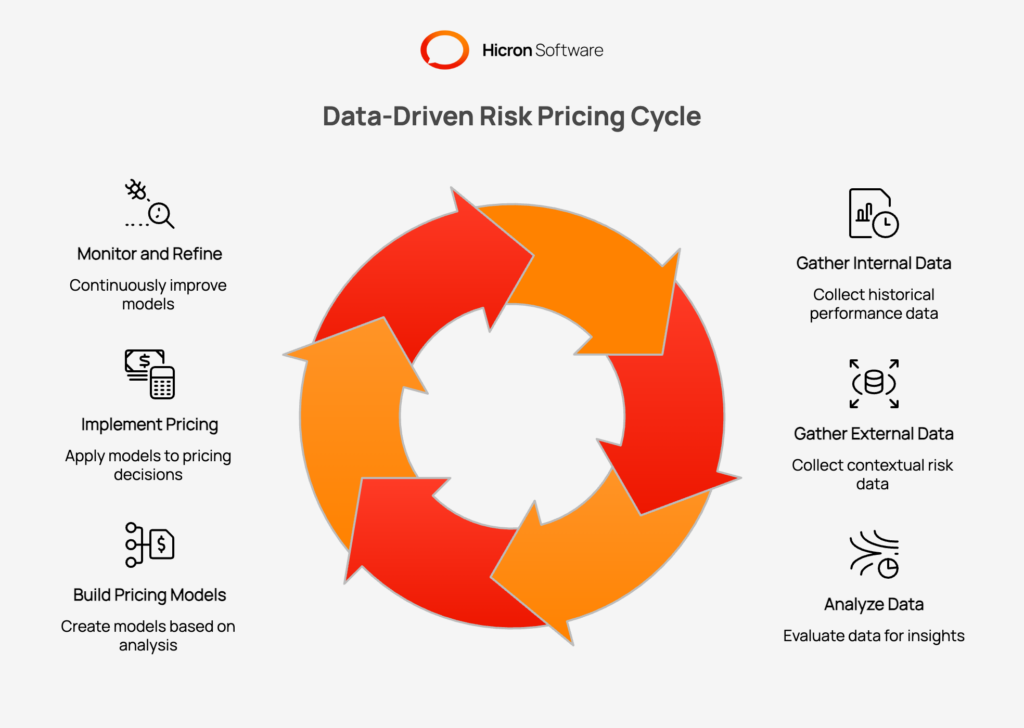

Data is the cornerstone of any effective risk based pricing system. The accuracy and relevance of your pricing models depend entirely on the quality of the information you use. The process starts with gathering a wide range of data. Internal data provides a historical view of performance. This includes customer profiles, transaction histories, claims records, and payment behaviors. This information offers direct insight into how different customer segments have performed in the past.

External data adds valuable context that internal sources alone cannot provide. Sources like credit bureau scores, public records, industry benchmarks, and economic indicators help create a more complete picture of risk. For instance, a small business’s credit history combined with data on its industry’s current market conditions allows for a more nuanced assessment. The quality of this data is central. Information should be clean, accurate, and up to date. Inaccurate or incomplete data will lead to flawed models, resulting in pricing that is either not competitive or not profitable. A robust data governance framework is necessary to maintain data integrity throughout its lifecycle. This ensures that the foundation of your risk assessment process is solid.

After collecting the necessary data, the next phase is to identify the specific variables that predict risk. This involves a detailed analysis to discover which factors have the strongest correlation with desired outcomes, such as loan repayment or low claims frequency. This is about using statistical methods to find genuine predictive signals within the data. Common risk factors in lending and insurance include:

However, each organization may find unique variables that are specific to its customer base and products.

Statistical models and machine learning algorithms are used to determine the relative importance of each factor. For example, a regression analysis can show how much a change in one variable, like credit score, affects the probability of a default. This process assigns a weight to each risk factor. This means that some factors will have a greater influence on the final risk score than others. A customer’s payment history might be a stronger predictor of future behavior than their geographic location, so it would receive a higher weight in the model. This analytical rigor ensures that the resulting risk scores are based on evidence, not assumptions. This step is critical for building a pricing model that accurately reflects the true risk of each customer.

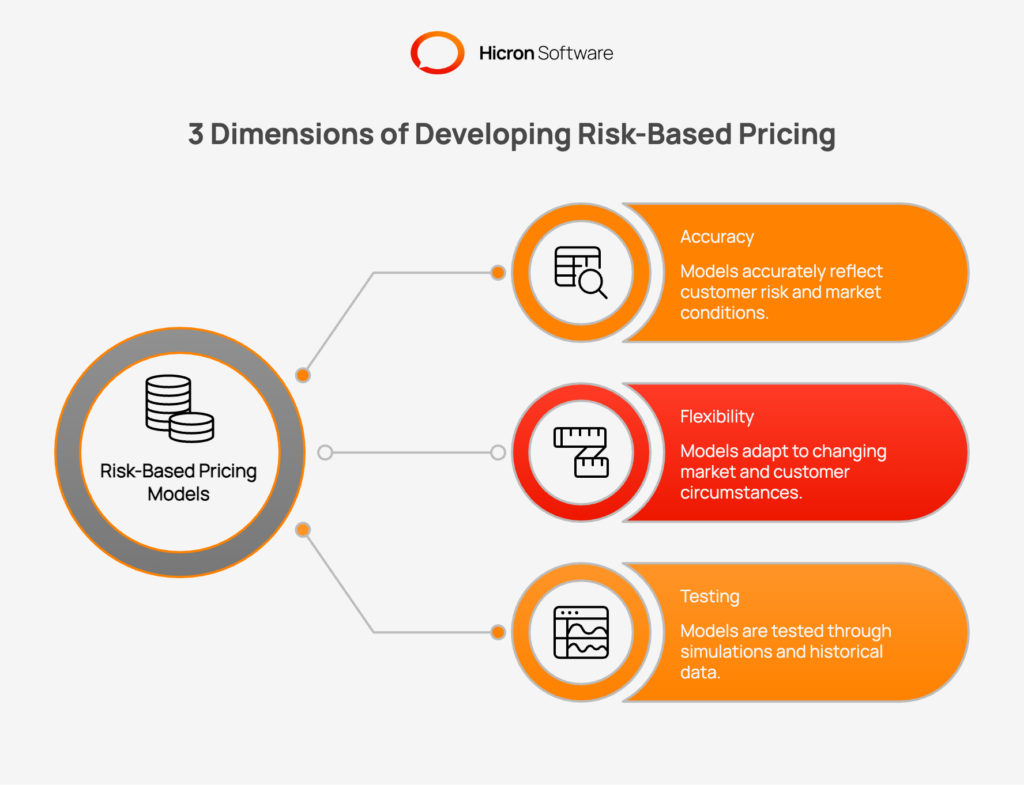

With a clear understanding of key risk factors, you can construct the pricing model itself. This model translates a customer’s calculated risk score into a specific price, such as an interest rate or an insurance premium. There are different methodologies for building these models. Traditional actuarial approaches use historical data and statistical tables to determine rates. These methods are reliable and well established. More modern approaches use predictive analytics and machine learning, which can analyze complex patterns in real time and adapt to changing conditions.

Flexibility is a key attribute of a strong pricing model. The market is not static, and customers’ circumstances can change. A rigid model that cannot accommodate exceptions may turn away good customers. For example, a system could be designed to allow underwriters to make adjustments for specific situations. A customer with a long, positive history with the company might warrant a better rate, even if one of their risk factors has recently changed.

Before a new model is implemented, it needs to be thoroughly tested. This is often done through simulations using historical data. The organization can see how the model would have priced past customers and whether it would have accurately predicted their performance. This validation process helps confirm that the model is not only accurate but also fair and compliant with regulations. It ensures the model will perform as expected when it is used with live customers.

An effective underwriting workflow balances speed with precision. The goal is to process applications efficiently while giving complex cases the attention they need. This is achieved by creating a segmented workflow that automatically handles straightforward applications and routes more complicated ones to human underwriters. This structure improves the customer experience by providing quick decisions when possible. It also allows your skilled team members to focus their expertise where it is most valuable.

A common approach involves creating different lanes for applications based on their initial risk assessment.

For this system to work, the rules governing it should be customizable. Underwriters may need the ability to adjust certain parameters based on the unique context of an application. For instance, an underwriter might look at additional documents or have a conversation with a small business owner to understand their specific situation better. This flexibility ensures that the process remains fair and can adapt to individual circumstances that an algorithm alone might misinterpret.

Modern risk-based pricing and underwriting are not possible without the right technology. Manual processes are too slow and prone to error to handle the volume and complexity of data involved. Technology provides the infrastructure to collect, analyze, and act on information quickly and at scale. Artificial intelligence and machine learning are at the forefront of this technological shift. These tools can analyze immense datasets to identify subtle patterns that humans might miss. They enable dynamic pricing, where rates can be adjusted in real time based on new information.

Application Programming Interfaces (APIs) are another crucial piece of the technological puzzle. APIs allow different software systems to communicate with each other. This enables your underwriting platform to pull data directly from credit bureaus, fraud detection services, and other third party sources. This automation reduces the need for manual data entry and ensures that underwriters are working with the most current information available.

Workflow automation platforms tie everything together. These tools manage the flow of applications through the underwriting process. They can handle tasks like sending notifications, requesting additional documents from customers, and ensuring that all necessary compliance checks are completed. By automating these routine administrative tasks, these platforms free up underwriters to concentrate on the more complex aspects of risk assessment. Choosing scalable technology is important for future growth, ensuring the system can handle an increasing volume of business.

|

Technology |

Description |

Benefits |

|

Artificial Intelligence (AI) & Machine Learning (ML) |

Advanced tools that analyze massive datasets to identify subtle patterns and trends that human analysis might overlook. |

• Enables dynamic, real-time pricing adjustments. |

|

Application Programming Interfaces (APIs) |

Connectors that allow different software systems to communicate, enabling direct data retrieval from third-party sources like credit bureaus and fraud detection services. |

• Eliminates manual data entry. |

|

Workflow Automation Platforms |

Centralized systems that manage the application lifecycle, handling administrative tasks such as notifications, document requests, and compliance checks. |

• Frees up underwriters to focus on complex cases. |

Implementing a risk-based pricing system carries with it a responsibility to ensure fairness and compliance with all applicable regulations. Financial services are highly regulated to protect consumers. Any pricing or underwriting model must adhere to laws designed to prevent unfair discrimination, such as the Equal Credit Opportunity Act (ECOA). This act prohibits credit discrimination on the basis of race, color, religion, national origin, sex, marital status, or age.

It is critical to test models for disparate impact. This occurs when a seemingly neutral policy has a disproportionately negative effect on a protected group. For example, if a model uses a geographic factor that closely correlates with the racial composition of a neighborhood, it could lead to discriminatory outcomes, even if race itself is not a variable in the model. Regular audits and statistical tests are necessary to identify and correct for such biases.

Transparency with customers is also essential for building trust. When an application is denied or a customer is offered a less favorable rate, they are entitled to know the reasons. Providing clear, specific explanations helps customers understand the decision. It also gives them information they can use to improve their financial situation. This practice meets regulatory requirements and demonstrates a commitment to fair and ethical business practices. Maintaining this focus on compliance and transparency is fundamental to the long-term viability of any risk-based pricing strategy.

A risk-based pricing and underwriting system is not a static product. It is a dynamic process that requires continuous monitoring and refinement. The market, customer behaviors, and regulatory requirements all change over time. A model that is accurate today may become less effective in the future. Therefore, a structured approach to testing and optimization is necessary.

The process often begins with a pilot program. A new workflow or pricing model can be rolled out to a limited segment of the business, such as a specific product line or geographic region. This allows the organization to observe how the system performs in a real-world environment without exposing the entire business to potential issues. Key performance indicators (KPIs) should be tracked closely during this phase. These metrics may include conversion rates, loss ratios, the time it takes to process an application, and customer satisfaction scores.

The data gathered from the pilot program provides the basis for iteration. If conversion rates are lower than expected, it might indicate that prices for low-risk customers are not competitive enough. If loss ratios are too high, the model may be underestimating risk. This feedback loop of testing, measuring, and refining is a continuous cycle. It ensures that the system remains aligned with business goals and adapts to the evolving environment. This commitment to ongoing improvement is what separates a good system from a great one.

Technology and data are only part of the equation. The people who use the system are just as important. The successful implementation of a new risk-based pricing workflow depends on the team’s ability and willingness to adopt it. Change can be met with resistance, especially if employees feel that automation threatens their roles. Proper training and support are essential to manage this transition smoothly.

Training should go beyond simply teaching people how to use the new software. It should explain the strategy behind the new system. When underwriters and pricing analysts understand why the changes are being made and how they will help the business, they are more likely to support the initiative. Training should show them how automation will handle repetitive tasks, allowing them to focus on more strategic work like analyzing complex cases and building relationships with clients.

Ongoing support is also vital. There should be a clear process for employees to ask questions and report problems. Creating a channel for feedback allows the team on the front lines to contribute to the system’s improvement. These individuals often have valuable insights that can help refine the process. Investing in your team ensures that you get the maximum value from your investment in technology. A well trained and supported team is a powerful asset in managing risk effectively.

Effective communication is critical for the successful rollout of any new business process. Changes to pricing and underwriting workflows affect many groups, so a comprehensive communication plan is needed. This plan should address both internal and external stakeholders.

Within the organization, all relevant departments should be informed about the changes. The executive team needs to understand how the new system aligns with strategic objectives. The sales team needs to be trained on the new pricing structure so they can communicate it clearly to customers. The compliance department needs to be involved from the beginning to ensure that all new processes meet regulatory standards. Clear internal communication prevents confusion and ensures that everyone is working toward the same goals.

External communication, primarily to customers, is also important. The changes should be framed in terms of benefits to them. For example, the new system can be presented as a way to receive faster decisions and more personalized rates. Transparency about how pricing is determined can help build trust. By managing communication proactively, an organization can ensure a smooth transition and maintain positive relationships with all its stakeholders. This helps realize the full benefits of the new risk based system.

Stay ahead of industry demands with advanced risk-based pricing and underwriting solutions. As the insurance sector evolves, organizations that implement data-driven, customizable systems are positioned for optimal efficiency and growth.

Hicron Software offers specialized expertise in designing robust frameworks that align with both regulatory standards and business objectives. We integrate proven technology with in-depth industry insight to deliver tailored systems that address your organization’s unique requirements.

Engage our team to develop an end-to-end risk-based pricing and underwriting platform that provides:

To discuss how a custom solution can help your organization achieve superior results, contact us to arrange a strategic consultation.

Risk based pricing is a strategy where lenders and insurers set the price of a product, such as a loan or insurance policy, based on the risk profile of the individual customer. Customers who are assessed as lower risk typically receive more favorable rates, while those assessed as higher risk receive less favorable rates.

Data quality is critical because the entire risk assessment process relies on it. Inaccurate, incomplete, or outdated data will lead to flawed risk models, which can result in mispriced products, financial losses, and unfair outcomes for customers.

Automation improves underwriting by handling routine, low-complexity applications quickly, often providing instant approvals for low risk customers. This increases efficiency, reduces operational costs, and allows skilled human underwriters to focus their time on complex cases that require judgment.

A manual review is reserved for applications that do not clearly fit into a low risk or high risk category. It allows an experienced underwriter to assess unique circumstances, consider additional information, and make a nuanced decision that an automated system might not be able to handle.

Organizations can ensure fairness by regularly testing their models for bias and disparate impact on protected groups. This involves statistical analysis to confirm that the model’s outcomes are equitable. Adhering to all regulatory requirements and being transparent with customers about decisions are also key components of maintaining a fair system.

Hicron Software proved to be a trusted partner with unmatched technical expertise, delivering a scalable and user-friendly web application that was pivotal to our successful U.S. market expansion.

Hicron’s contributions have been vital in making our product ready for commercialization. Their commitment to excellence, innovative solutions, and flexible approach were key factors in our successful collaboration.

I wholeheartedly recommend Hicron to any organization seeking a strategic long-term partnership, reliable and skilled partner for their technological needs.

After carefully evaluating suppliers, we decided to try a new approach and start working with a near-shore software house. Cooperation with Hicron Software House was something different, and it turned out to be a great success that brought added value to our company.

With HICRON’s creative ideas and fresh perspective, we reached a new level of our core platform and achieved our business goals.

Many thanks for what you did so far; we are looking forward to more in future!

Hicron is a partner who has provided excellent software development services. Their talented software engineers have a strong focus on collaboration and quality. They have helped us in achieving our goals across our cloud platforms at a good pace, without compromising on the quality of our services. Our partnership is professional and solution-focused!

The IT system supporting the work of retail outlets is the foundation of our business. The ability to optimize and adapt it to the needs of all entities in the PSA Group is of strategic importance and we consider it a step into the future. This project is a huge challenge: not only for us in terms of organization, but also for our partners – including Hicron – in terms of adapting the system to the needs and business models of PSA. Cooperation with Hicron consultants, taking into account their competences in the field of programming and processes specific to the automotive sector, gave us many reasons to be satisfied.