How to Integrate InsurTech with Legacy Systems? Technology Integration Guide

- April 29

- 11 min

Legacy system modernization in insurance involves updating outdated technology systems to improve efficiency, scalability, and customer experience. It replaces or enhances old systems with modern solutions like cloud computing, AI, and APIs to streamline operations and integrate with new technologies. This transformation helps insurers reduce costs, mitigate risks, and stay competitive in a rapidly evolving market.

You’ll learn how legacy modernization services in insurance drive efficiency, enhance customer satisfaction, and unlock opportunities through the use of AI, cloud computing, and automation. Additionally, explore the modern insurance system’s technology and how leading insurers are adapting to this transformation to future-proof their businesses. By the end, you’ll understand why modernizing legacy systems in insurance is an opportunity to thrive in the digital insurance era.

Legacy systems refer to older computing software, hardware, or technology infrastructure that an organization continues to use despite the availability of newer, more efficient alternatives. In the context of the insurance industry, these systems in the insurance industry often serve as the backbone for critical functions like policy administration and claims management. While they may still handle daily tasks, they typically rely on older programming languages and architecture that modern developers no longer support. As a result, maintaining these insurance legacy systems becomes increasingly expensive and risky over time.

For many insurance companies, these platforms were implemented decades ago. Over time, layers of patches and ad-hoc fixes have created a complex web of dependencies, often referred to as spaghetti code. This outdated legacy technology creates silos where data is trapped, making it difficult for an insurer to get a unified view of their business or their clients. The rigidity of a legacy insurance system prevents agility, slowing down the launch of new products and hindering the integration of third-party digital tools. Consequently, relying on such infrastructure can severe limit an organization’s ability to compete in a digital-first market.

The push for insurance legacy system transformation is driven by rapidly changing market trends and consumer behaviors. Today’s policyholders expect instant service, personalized offers, and mobile-first interactions. An outdated legacy system cannot support the real-time data processing required to meet these demands. When an insurer relies on slow, batch-processing mainframes, they fail to provide the responsiveness that modern customers demand. This gap between customer expectation and technological capability is where modernized competitors steal market share.

Furthermore, regulatory compliance and security risks are escalating. Older systems often lack the robust security features found in modern insurance technology, making them vulnerable to cyber threats. Additionally, as regulations evolve, updating hard-coded rules in a core legacy system can be a nightmare of manual effort and testing. Transforming legacy infrastructure is no longer just about upgrading technology; it is a survival imperative. Insurance legacy system transformation becomes the catalyst for business resilience, ensuring that an insurer can adapt to new laws, protect customer data, and pivot quickly when market dynamics shift.

The insurance industry is undergoing a rapid technological transformation, yet many companies remain anchored to aging legacy systems.

Below, we’ll explore the critical pain points of relying on legacy systems and how solutions like modernization services can help insurers overcome these obstacles.

|

Challenge |

Description |

Example/Impact |

|

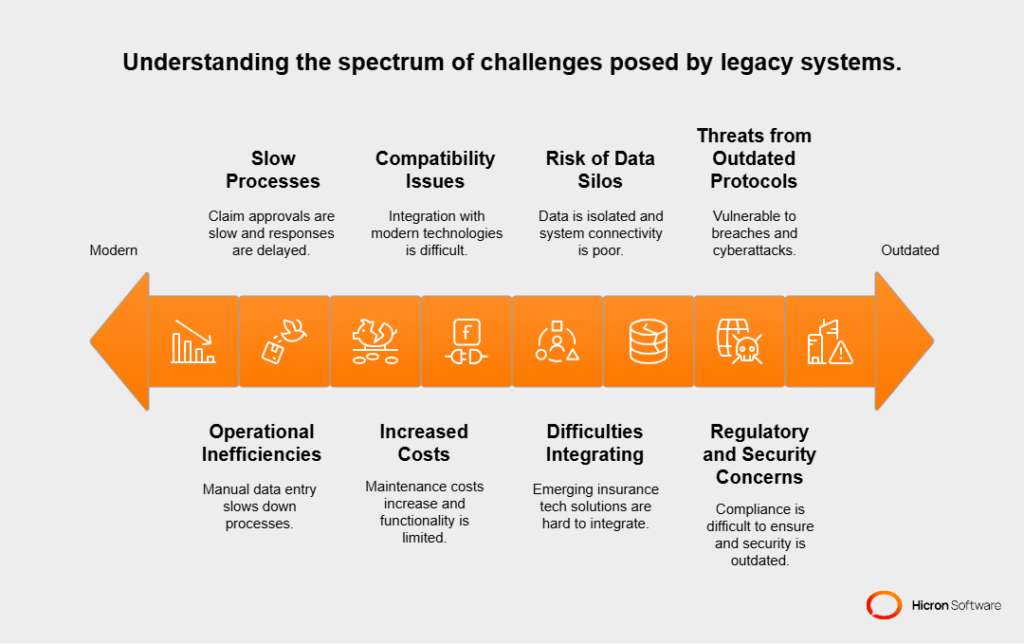

Operational inefficiencies caused by outdated systems |

Legacy systems lack speed, flexibility, real-time data processing, and automation, leading to bottlenecks and reduced productivity. |

Manual data entry and outdated workflows slow down underwriting and claims management, making it hard to compete with agile insurtech startups. |

|

Slow processes reducing customer satisfaction |

Legacy systems result in slow claim approvals, delayed responses, and cumbersome policy management, frustrating customers. |

A life insurance applicant might wait weeks for an underwriting decision, leading to dissatisfaction, while insurtech companies deliver decisions in minutes using automation. |

|

High costs of maintaining legacy systems |

Maintenance costs rise as systems age, requiring scarce expertise and draining budgets that could be used for innovation. |

Legacy systems lack functionality for advancements like AI or automation, forcing insurers to invest in outdated infrastructure instead of modern technologies. |

|

Compatibility issues with modern technologies |

Legacy systems are rigid and difficult to integrate with emerging technologies like AI, telematics, or digital claims management. |

Insurers face challenges implementing telematics for usage-based insurance or automated claims systems, putting them at a disadvantage compared to insurtech startups. |

|

Challenges in integrating modern tech solutions |

Legacy systems resist integration with IoT, AI, and predictive analytics, making innovation costly and complex. |

Implementing AI for claims processing or predictive analytics for risk assessment becomes a resource-intensive endeavor. |

|

Risks of data silos and poor connectivity |

Legacy systems create isolated data silos, hindering communication and collaboration across departments. |

A commercial insurance team may struggle to access unified customer data when policies are spread across multiple platforms, leading to inefficiencies and missed opportunities. |

|

Regulatory and security concerns |

Legacy systems lack flexibility to adapt to regulatory changes, leaving insurers vulnerable to compliance issues, fines, and reputational damage. |

Evolving data privacy laws require systems that can quickly adjust to new standards, which legacy systems struggle to meet. |

|

Threats from outdated security protocols |

Legacy systems rely on outdated security protocols, making them vulnerable to cyberattacks and data breaches. |

Hackers can exploit vulnerabilities in aging infrastructure, compromising sensitive customer data. Upgrading to modern systems with advanced security features is essential to protect data and reputation. |

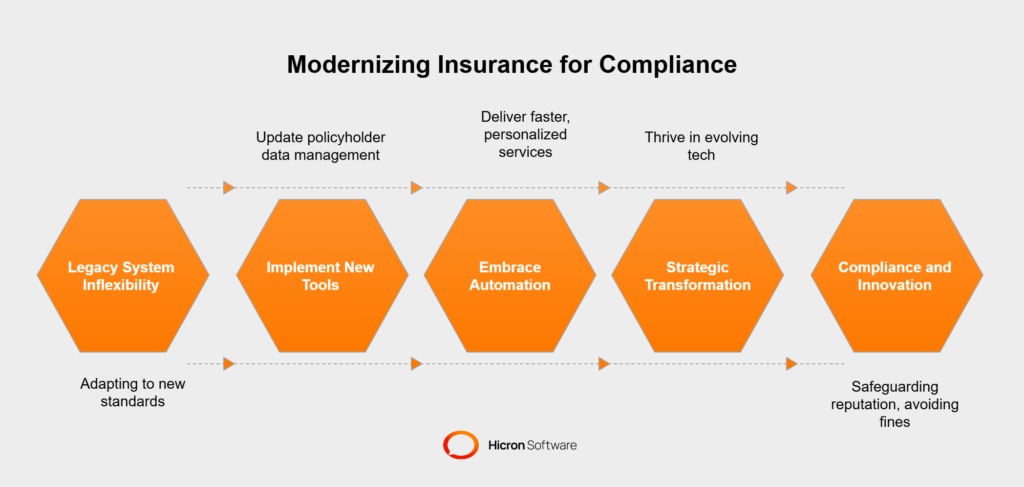

Compliance in the insurance industry is a constantly moving target. New data standards, privacy laws, and industry regulations emerge regularly, requiring insurers to adapt quickly. Unfortunately, insurance legacy systems were designed long before modern compliance frameworks. They often lack the flexibility to meet these evolving demands.

This inability to adapt not only risks regulatory penalties but also erodes customer trust. Through legacy system modernization in insurance, insurers can ensure compliance with current and future standards, safeguard their reputation, and avoid costly fines.

Customer experience is the main battleground for insurance providers today. Unfortunately, legacy systems in the insurance sector often act as a barrier to delivering excellent service. When a customer calls with a question, agents often have to toggle between multiple screens and disjointed databases to find an answer. This friction leads to long wait times and frustration. Without digital self-service tools linked to a modern core system, customers cannot easily check policy status or file claims online, forcing them into slower, manual channels that damage customer satisfaction.

The inability to access real-time data prevents insurance companies from offering personalized advice or usage-based pricing models. A legacy system usually processes data in batches overnight, meaning an insurer is always looking at yesterday’s information.

In contrast, modernizing legacy systems enables a 360-degree view of the customer. This allows for proactive engagement, such as automated renewal reminders or personalized risk mitigation tips. Ultimately, upgrading legacy systems is the only way to build the fluid, responsive journey that retains clients in a competitive landscape.

The benefits of insurance legacy system modernization are extensive, directly impacting the bottom line.

First and foremost is the boost in operational efficiency. By automating manual workflows that were previously stuck in paper-based or manual processes, employees can focus on high-value tasks rather than data entry. Modern systems allow for streamlined insurance processes, reducing the time it takes to underwrite a policy or settle a claim. This speed pleases customers and reduces administrative overhead for the insurer.

Another major advantage is the reduction of technical debt. Maintaining aging legacy infrastructure requires specialized skills that are becoming rare and expensive. By replacing legacy systems or upgrading them, companies can reduce costs associated with maintenance and server hardware.

A modern insurance system is built for connectivity. It allows for easy integration with API ecosystems, enabling insurers to partner with insurtechs, access new distribution channels, and launch innovative products faster. This agility is the primary reward of a successful insurance legacy system transformation.

Artificial intelligence (AI) and automation are the engines of growth for a modern insurer, but they require a solid technical foundation to function. Legacy modernization opens the door to these advanced capabilities. Once data is freed from siloed mainframes, AI algorithms can analyze vast amounts of information to identify patterns that humans might miss. For instance, AI can detect fraudulent activity in real-time during the claims process, saving the industry billions annually. This level of sophistication is virtually impossible with an outdated legacy system.

Automation goes hand in hand with AI to transform insurance operations. Routine tasks, such as document verification or initial risk assessment, can be fully automated, ensuring consistency and speed. A modern insurance system allows for “straight-through processing”. Simple claims are adjudicated and paid without human intervention. This shifts the role of insurance agents and claims adjusters from processors to advisors.

By modernizing legacy insurance platforms, companies can use AI to predict customer needs, tailor coverage, and dynamically optimize pricing, creating a truly modern insurance offering.

Choosing the right path is crucial, and there are several modernization strategies available. One common method is a complete replacement, often called “rip and replace.” This involves retiring the existing system entirely and implementing a new insurance software package. While this offers a fresh start with the latest features, it carries high risk and cost.

Another approach is “encapsulation,” where the legacy system’s architecture is wrapped in a modern interface (API layer). This allows modern applications to interact with the old data and logic, extending the life of the system without touching the core legacy code.

Many insurance companies prefer a phased system migration. This modular approach involves modernizing specific components, like the policy administration system or billing module, one at a time. This reduces the risk of system failures and allows the business to see incremental value.

Re-platforming, or “lift and shift,” involves moving the application to the cloud with minimal changes. This helps reduce infrastructure costs but may not solve underlying functional issues. The most effective insurance legacy system strategy often involves a hybrid of these approaches to modernization, tailored to the specific risk appetite and budget of the organization.

Insurance data modernization is often the most complex part of the journey. Legacy systems in insurance hold decades of historical records. But this legacy data is often messy, duplicated, or stored in incompatible formats. Simply moving bad data to a new system will not yield results. Modernizing legacy applications and data requires a strategy for data cleansing and migration. Insurers must define what data is essential to migrate and what can be archived.

The goal is to transform this raw information into a strategic asset. By migrating to a cloud-native database, insurance data becomes accessible and scalable. This enables advanced analytics and business intelligence. Real-time data access empowers decision-makers to spot market shifts instantly. Transforming legacy data ensures compliance with modern privacy regulations like GDPR. Without a focus on data quality, even the most expensive digital transformation will fail to deliver the expected insights.

The road to modernization in insurance is fraught with challenges. One of the biggest hurdles is the fear that the system might crash during the transition, disrupting business continuity. These systems are mission-critical; a failure in the claims processing system or policy engine can halt revenue and damage reputation. Additionally, documentation for legacy technology is often missing or outdated, making it difficult for new developers to understand the logic embedded in the code.

Cultural resistance is another obstacle. Employees who have used the same green-screen interface for twenty years may resist adopting new digital insurance tools. Managing this change requires training and communication. Budget overruns are also common, as the complexity of untangling legacy data and platforms often exceeds initial estimates. To help insurance companies succeed, leadership should view this not as a one-time IT project, but as a continuous evolution of the business model.

Building an effective insurance legacy system modernization strategy starts with a clear assessment of current capabilities and future goals. Leaders should audit their legacy systems to understand the technical debt and business impact of each component. It is vital to align the technology roadmap with business objectives, whether that is to enter new markets, improve customer experience, or cut costs. This alignment ensures that modernization efforts deliver tangible value.

Selecting the right partner is also essential. Insurers need technology partners who understand the nuances of the insurance sector and have experience with complex system modernization. The strategy should prioritize “quick wins” to demonstrate value early to stakeholders.

For example, upgrading the customer-facing portal before tackling the core backend can improve customer satisfaction quickly. A successful insurance legacy system strategy is flexible, allowing the insurer to adjust course as technology and market conditions evolve.

The future of the insurance industry lies in connected, intelligent ecosystems. Once the heavy lifting of insurance legacy system transformation is complete, insurers can focus on innovation. We will see the rise of usage-based insurance models driven by IoT devices and telematics, where premiums are based on real-time behavior. Modern systems will enable “embedded insurance,” where coverage is sold as an add-on to other products and services.

Legacy and modern systems may coexist for a time, but the trajectory is clear: a move toward cloud-native, AI-driven platforms. These modern systems will be self-updating and infinitely scalable. The focus will shift from processing policies to preventing losses. With modernization for insurance complete, the insurer becomes a proactive partner in their customer’s life, using data to predict risks and offer protection before a loss occurs. Transforming insurance legacy systems is the gateway to this future.

Legacy insurance system modernization is a strategic investment in innovation, resilience, and long-term success. To explore practical steps and tailored strategies for upgrading your systems, connect with industry experts who can guide you through the transformation. Together, we can build a stronger, smarter, and more agile future for the insurance industry.

The biggest risk is operational disruption. If the migration is not planned correctly, critical functions like claims processing or policy issuance could fail, leading to financial loss and reputational damage. Data loss or corruption during migration is also a major concern.

The timeline varies wildly depending on the scope. A full “rip and replace” of a core system can take 2 to 5 years. However, a phased approach focusing on specific modules or using encapsulation might deliver results in 12 to 18 months.

Direct integration is difficult. Legacy systems often lack the APIs required for modern AI tools. However, using an encapsulation strategy (wrapping the legacy system in an API layer) can allow AI applications to access and analyze legacy data without a full system replacement.

Data is an insurer’s most valuable asset. Legacy systems often store data in silos or obsolete formats. Modernizing this data allows for better risk modeling, personalized marketing, and accurate fraud detection, which are impossible with disorganized legacy data.

Digitization usually refers to converting analog information (paper) into digital formats. Modernization refers to updating the underlying IT infrastructure and software architecture (legacy systems) to improve performance, scalability, and flexibility.

Incremental modernization is a phased approach where insurers upgrade high-impact areas (e.g., claims processing or policy management) first, rather than overhauling the entire system at once. This method minimizes disruption, reduces risk, and ensures steady progress toward a fully modernized technology stack.

Modern systems enable insurers to:

These improvements lead to higher customer satisfaction and loyalty.

Insurers that fail to modernize risk:

The timeline for modernization depends on the scope of the project. Incremental modernization (focusing on specific areas first) can take a few months, while a full system overhaul may take 1-2 years. Partnering with experienced insurance software developers can help streamline the process and reduce implementation time.

To ensure success, insurers should:

Hicron Software proved to be a trusted partner with unmatched technical expertise, delivering a scalable and user-friendly web application that was pivotal to our successful U.S. market expansion.

Hicron’s contributions have been vital in making our product ready for commercialization. Their commitment to excellence, innovative solutions, and flexible approach were key factors in our successful collaboration.

I wholeheartedly recommend Hicron to any organization seeking a strategic long-term partnership, reliable and skilled partner for their technological needs.

After carefully evaluating suppliers, we decided to try a new approach and start working with a near-shore software house. Cooperation with Hicron Software House was something different, and it turned out to be a great success that brought added value to our company.

With HICRON’s creative ideas and fresh perspective, we reached a new level of our core platform and achieved our business goals.

Many thanks for what you did so far; we are looking forward to more in future!

Hicron is a partner who has provided excellent software development services. Their talented software engineers have a strong focus on collaboration and quality. They have helped us in achieving our goals across our cloud platforms at a good pace, without compromising on the quality of our services. Our partnership is professional and solution-focused!

The IT system supporting the work of retail outlets is the foundation of our business. The ability to optimize and adapt it to the needs of all entities in the PSA Group is of strategic importance and we consider it a step into the future. This project is a huge challenge: not only for us in terms of organization, but also for our partners – including Hicron – in terms of adapting the system to the needs and business models of PSA. Cooperation with Hicron consultants, taking into account their competences in the field of programming and processes specific to the automotive sector, gave us many reasons to be satisfied.