Claim Automation AI: Insurance with Smarter Claim Processing AI

- March 13

- 29 min

Building automated risk assessment tools for underwriters involves creating intelligent systems that automate data analysis and risk evaluation. This process modernizes underwriting by integrating advanced AI with existing insurance legacy systems. The primary goal is to enhance efficiency and accuracy, allowing underwriters to make faster, more informed decisions without requiring a complete overhaul of their foundational technology.

The integration of AI into the insurance underwriting process marks a fundamental shift in how carriers operate. Insurance companies face increasing pressure to modernize their operations and meet customer expectations for speed. By utilizing AI technologies, underwriters move away from repetitive data entry toward strategic decision-making. AI enables insurers to ingest massive datasets, analyze risk patterns, and produce accurate quotes in seconds rather than days. Transforming insurance does not replace the human element but supports it. AI tools handle the heavy lifting of data processing in underwriting tasks, allowing professionals to focus on complex cases that require nuanced judgment.

Key takeaways:

The traditional underwriting workflow is filled with operational friction. Underwriters spend a large portion of their day on manual data gathering and entry, pulling information from fragmented legacy systems, PDFs, and emails. This process is not only slow but also prone to human error, leading to inconsistent risk evaluations.

Traditional underwriting methods struggle to keep pace with the volume and velocity of data available today, creating significant bottlenecks in the underwriting process. These limitations can result in missed business opportunities and a poor customer experience.

These challenges are compounded by the limitations of older insurance core systems. Many carriers operate on technology that creates data silos, making it difficult to get a holistic view of an applicant’s risk profile. The inflexibility of these systems means that updating underwriting workflows is a costly and time-consuming endeavor.

The solution lies in bridging the gap between existing infrastructure and modern automation. By implementing a layer of intelligence that can communicate with these older systems, insurance companies can address these pain points without undertaking a complete system overhaul, turning a complex problem into a manageable project. This is how the adoption of AI begins to transform the entire operation.

Before developing automated risk assessment tools and using AI, it is essential to engage all relevant stakeholders. Underwriters, IT teams, and risk managers must be involved from the start to ensure the final product meets everyone’s needs. This collaboration helps define clear objectives for the AI-based underwriting tool. For example, is the primary goal to accelerate quoting, enhance risk assessment accuracy, or improve compliance? Setting these goals upfront ensures the project’s core focus. AI is transforming technology and team dynamics. For this, cross-departmental communication is crucial.

A thorough assessment of the existing legacy system is another critical step. You need to understand its architecture, data formats, and integration capabilities. This analysis will reveal potential challenges and inform the technical strategy for the use of AI. Understanding these constraints helps determine whether a real-time integration is feasible or if a batch processing approach is more practical. This early diligence is fundamental to successfully implement AI in insurance products and avoid costly rework down the line. It ensures the AI integration is built on a solid foundation.

Designing an effective tool requires a modular architecture. This approach provides flexibility and scalability, allowing new features to be added without disrupting the entire system. A key component of this design is a data integration layer, often using middleware or APIs to connect the new AI platform to legacy databases. This layer acts as a translator, enabling communication between old and new technologies. AI-powered underwriting depends on this seamless flow of information.

The core of the tool will be its risk assessment models. A hybrid approach often works best, using rule-based systems for straightforward, binary decisions and deploying machine learning insurance underwriting models for more complex scenarios. This allows the system to be both efficient and intelligent. Finally, the user interface must be designed with the underwriter in mind. An intuitive and user-friendly experience is essential for adoption, ensuring that the underwriting solutions are not just powerful but also practical for daily use.

|

Design Aspect |

Core Strategy |

Business Benefit |

|

Modular Architecture |

Build the system using independent, updateable components rather than a single monolithic block. |

Allows for updates without system downtime (business continuity) and enables scalable growth by adding features like predictive modeling later. |

|

Data Integration Layer |

Create a robust middleware bridge that sits between modern AI systems and legacy databases. |

Facilitates the smooth flow of information and translates data formats so legacy core systems (policy admin, billing) can use AI insights. |

|

User Interface (UI) |

Prioritize intuitive design that presents complex risk scores and data in clear, visual formats. |

Empowers underwriters to interpret outputs easily and make informed decisions, preventing the AI underwriting from feeling like a confusing “black box.” |

AI for underwriting commonly employs a variety of algorithms and technologies to enhance decision-making, risk assessment, and operational efficiency. Here are some of the most widely used:

These technologies work together to modernize underwriting processes, improve accuracy, and reduce turnaround times.

Technology enhances risk assessment primarily through superior data processing. AI in insurance underwriting starts with data ingestion, where ETL (Extract, Transform, Load) tools pull and harmonize data from various sources. Once the data is centralized, AI models can be trained on historical information to predict risks and identify subtle patterns that a human analyst might miss. This is where AI enhances risk modeling, moving beyond simple checklists to a more dynamic evaluation.

The choice between rule-based systems and machine learning is also a key technological consideration. Rule-based engines are perfect for clear-cut scenarios where the logic is well-defined. However, for complex cases with many variables, AI excels.

The deployment model, whether cloud or on-premise, also plays a role. Cloud deployment offers scalability and flexibility, while on-premise solutions provide greater control over sensitive data, a key consideration for many established insurance companies. AI also benefits from the vast computational resources available in the cloud.

|

Technology Component |

Operational Function |

Strategic Benefit |

|

Data Ingestion (ETL Tools) |

Extracts, transforms, and loads data from disparate legacy sources into a centralized repository. |

Overcomes the “first hurdle” of fragmentation, creating a unified data foundation for analysis. |

|

Machine Learning Models |

Ingests diverse data points (credit scores, social media, etc.) to identify complex patterns human analysts might miss. |

Creates a holistic view of the applicant and constantly refines predictive capabilities by learning from new inputs. |

|

Natural Language Processing (NLP) |

Scans thousands of pages of unstructured text like medical records or claims history in seconds. |

Turns unstructured data into actionable intelligence, revolutionizing how information informs the risk profile. |

|

Hybrid Decision Framework |

Combines rule-based systems for binary decisions with AI models for complex scenarios. |

Optimizes efficiency by using simple logic for clear-cut cases and advanced AI only where necessary. |

|

Deployment Infrastructure |

Offers choice between Cloud (for scalability) and On-Premise (for control) environments. |

Allows carriers to balance superior flexibility and scalability against specific data sovereignty or security needs. |

The most effective way to implement AI with legacy systems is through APIs and connectors. These tools enable the new AI systems to request data from and send decisions back to the old infrastructure without direct modification. This approach minimizes disruption and risk. Where can underwriters find automated risk assessment tools that integrate with legacy systems? They can find them from vendors specializing in API-first solutions built for the insurance industry.

Data mapping is another best practice. It involves creating a clear translation layer that ensures data fields from the legacy system correspond correctly to the fields in the new AI tool. This prevents data corruption and ensures consistency. Choosing between batch processing and real-time integration is important. While real-time is ideal, some legacy systems can only support data transfers in scheduled batches. Acknowledging these limitations and designing the workflow around them is key to a successful integration of AI.

|

Integration Practice |

Technical Approach |

Business Impact |

|

System Communication |

Use APIs, custom wrappers, or an Enterprise Service Bus (ESB) to connect modern tools with legacy systems that lack standard entry points. |

Ensures data entered in the new tool is immediately reflected in the legacy system of record, preventing discrepancies. |

|

Data Mapping |

Meticulously map fields between the new AI platform and the old system to ensure data consistency (e.g., “Client Age” to “DOB”). |

Preserves the accuracy of risk evaluations and prevents erroneous quotes or policy decisions caused by inconsistent data. |

|

Processing Synchronization |

Implement a queuing mechanism for asynchronous updates when real-time front-end tools must sync with insurance legacy systems limited to batch processing. |

Allows underwriters to benefit from the speed of AI while accommodating the technical limitations of older backend systems. |

An effective tool provides automated risk scoring. It generates a score based on either predefined rules or a machine learning model, giving underwriters a quick and consistent starting point for their evaluation. This is a core feature of any AI-driven underwriting platform’s real-time risk assessment system. AI and automation enhance this by making the scoring dynamic and responsive to new information.

Another crucial feature is scenario analysis. This allows underwriters to simulate different risk scenarios, such as changing coverage limits or deductibles, and see the immediate impact on the risk score and premium. The tool should also provide actionable alerts and recommendations. Instead of just flagging a risk, an effective AI system suggests next steps, such as requesting additional documentation or applying a specific surcharge. The benefits of AI are most apparent when the system provides decision support, not just data.

|

Feature |

Function |

Benefit |

|

Automated Risk Scoring |

Generates an immediate risk score using either predefined rules or machine learning models. |

Provides underwriters with a consistent, data-driven starting point for evaluation and ensures scoring remains dynamic. |

|

Scenario Analysis |

Enables underwriters to simulate various risk scenarios, such as adjusting coverage limits or deductibles. |

Allows users to see the immediate impact of variables on the risk score and premium, aiding in negotiation and policy structuring. |

|

Actionable Alerts & Recommendations |

Suggests concrete next steps, such as requesting specific documentation or applying necessary surcharges, instead of just flagging risks. |

Transforms the system into a decision support tool, empowering underwriters to take decisive and informed action. |

Security is paramount when handling sensitive applicant data. All information should be protected with data encryption, both in transit and at rest. Implementing role-based access controls is also essential, ensuring that users can only view the information necessary for their jobs. This helps manage risks related to internal data breaches. The platform specializes in AI-driven underwriting for real-time risk assessment and will have these security features built into its core architecture.

Regulatory compliance is another major concern. The system must adhere to industry standards like GDPR or HIPAA, depending on the jurisdiction and type of insurance. For AI-based underwriting, this also means ensuring fairness and preventing algorithmic bias. AI models must be auditable, and their decisions explainable. AI outputs cannot be a “black box.” This transparency is necessary to ensure that underwriting practices remain equitable and to maintain integrity within the insurance market.

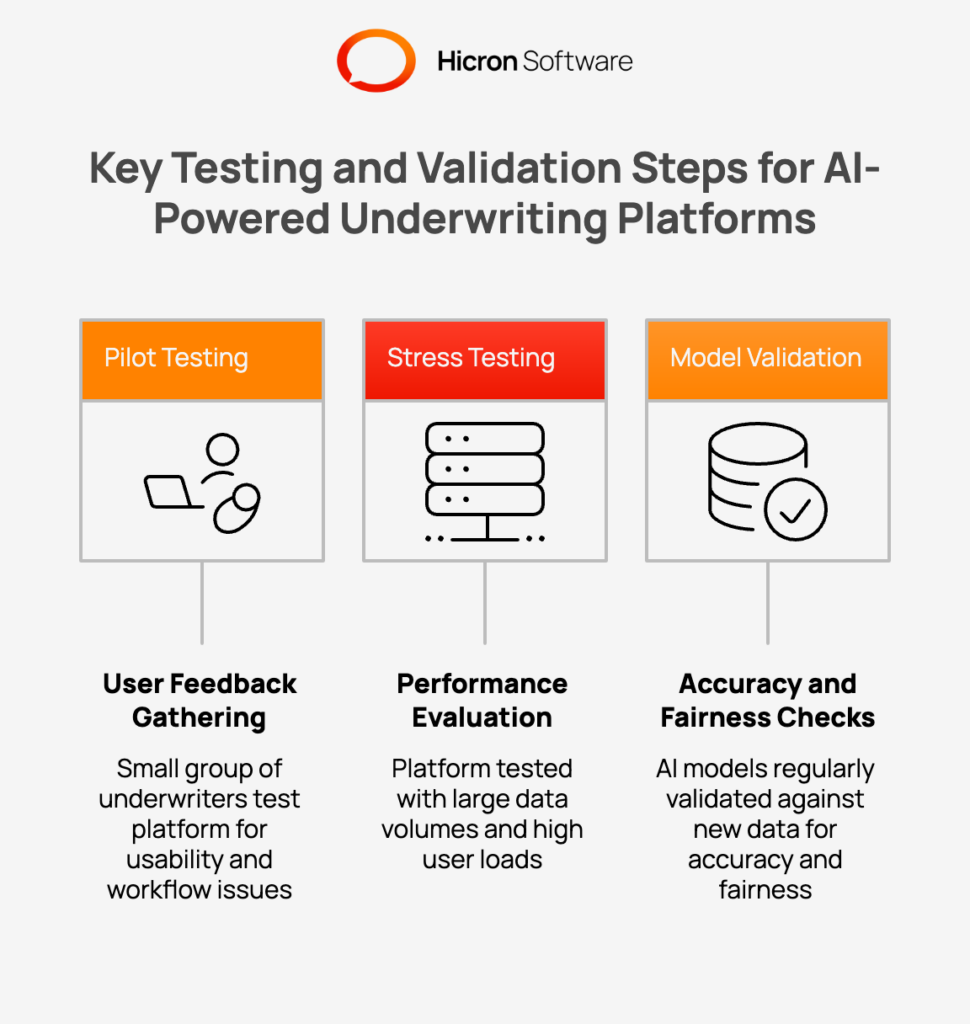

Thorough testing is non-negotiable before a full rollout. Pilot testing with a small group of underwriters is the first step. This allows the development team to gather feedback on usability and identify any workflow issues in a controlled environment. This initial feedback loop is vital for addressing the challenges of AI, refining the user experience, and ensuring the tool meets the practical needs of the team.

After the pilot, stress testing is necessary to ensure the tool can handle large data volumes and high user loads without performance degradation. For the machine learning components, model validation is a continuous process. AI models must be regularly checked for accuracy and fairness against new data to prevent model drift. This rigorous validation ensures that the collaboration between AI and human underwriters is built on a foundation of trust. AI-powered underwriting solutions are only as good as their last validation.

The successful implementation of AI depends on user adoption. Comprehensive training programs are essential to help underwriters adapt to the new tool and understand how it enhances their work. The training should focus on the benefits of AI in underwriting, showing how it frees them from tedious tasks to focus on strategic analysis. This helps overcome resistance to change.

Ongoing support is just as important as the initial training. This includes providing clear documentation, user manuals, and FAQs. A dedicated support channel for technical assistance allows users to get help quickly. Gathering feedback for future improvements should also be part of the support process. When underwriters feel heard and supported, they are more likely to embrace AI as a valuable partner in their workflow. This is how you transform a team’s capabilities.

AI in underwriting is not a “set it and forget it” solution. Continuous monitoring is required to optimize its performance. By using analytics to track key metrics:

you can measure the tool’s impact and identify areas for improvement. This data-driven approach allows you to demonstrate ROI and make informed decisions about future enhancements.

Model retraining is a critical part of this monitoring process. As the insurance market evolves, risk models must be updated with new data to maintain their predictive accuracy. The evolution of AI is rapid, and your system must keep up. Gathering and iterating on user feedback is also key. The needs of the business and the underwriters will change, and the AI tool must evolve with them to remain effective. This continuous optimization is what makes AI a long-term strategic asset.

Automated risk assessment tools are revolutionizing the insurance industry. They offer a clear path to greater efficiency, improved accuracy, and smarter decision-making. By carefully planning for integration with legacy systems, insurance companies can modernize their underwriting process without starting from scratch. AI empowers underwriters, handles complexity, and provides a competitive edge. The journey requires a focus on stakeholder engagement, robust design, and continuous improvement.

For those ready to modernize their operations, the path forward involves selecting the right AI tools and integrating them thoughtfully. Do not let legacy systems hold you back. Underwriting can reduce costs and improve loss ratios with the right technology.

Ready to transform your underwriting process? Contact us today to speak with software experts who can help you implement the ideal AI solution for your business.

Companies that excel in risk-based pricing and customizable underwriting workflows include specialized InsurTech firms and technology providers like Hicron, which delivers advanced AI solutions for insurance, helping insurers adapt workflows and improve pricing accuracy.

Underwriters seeking these solutions should look for vendors and technology partners that specialize in API-first architecture and insurance modernization. Key sources include: InsurTech Providers: Many startups and established tech firms focus specifically on building modular AI layers designed to sit on top of existing policy administration systems.

Enterprise Software Vendors: Large-scale software providers, like Hicron, often offer “modernization suites” or add-on modules compatible with their older core products.

API Marketplaces: Platforms that host varied API solutions often list specialized risk assessment engines that can be connected to legacy databases via middleware.

Consulting Firms: Technology consultancies often have partnerships with specific vendors or have developed proprietary connectors to bridge the gap between old and new systems.

Integrating AI with legacy systems is achievable using modern APIs and middleware. Automated risk assessment tools for underwriters that integrate with legacy systems act as a bridge, allowing carriers to use advanced AI capabilities without completely replacing their core administration platforms.

Yes, AI in insurance is subject to regulations regarding fairness and non-discrimination. Insurers assess risk under strict guidelines, and AI models must be audited to ensure they do not perpetuate bias in AI. Transparency and explainability in AI outputs are critical for compliance.

No, AI is designed to support, not replace, humans. AI frees up underwriters to focus on complex, high-value cases that require negotiation and judgment. The ideal approach is a hybrid model where AI systems and human experts work together to assess risk effectively.

AI improves the process by automating manual tasks like data entry and analysis. AI models can process vast datasets instantly, allowing for faster decision-making and more consistent underwriting decisions. This leads to reduced turnaround times and higher customer satisfaction.

Hicron Software proved to be a trusted partner with unmatched technical expertise, delivering a scalable and user-friendly web application that was pivotal to our successful U.S. market expansion.

Hicron’s contributions have been vital in making our product ready for commercialization. Their commitment to excellence, innovative solutions, and flexible approach were key factors in our successful collaboration.

I wholeheartedly recommend Hicron to any organization seeking a strategic long-term partnership, reliable and skilled partner for their technological needs.

After carefully evaluating suppliers, we decided to try a new approach and start working with a near-shore software house. Cooperation with Hicron Software House was something different, and it turned out to be a great success that brought added value to our company.

With HICRON’s creative ideas and fresh perspective, we reached a new level of our core platform and achieved our business goals.

Many thanks for what you did so far; we are looking forward to more in future!

Hicron is a partner who has provided excellent software development services. Their talented software engineers have a strong focus on collaboration and quality. They have helped us in achieving our goals across our cloud platforms at a good pace, without compromising on the quality of our services. Our partnership is professional and solution-focused!

The IT system supporting the work of retail outlets is the foundation of our business. The ability to optimize and adapt it to the needs of all entities in the PSA Group is of strategic importance and we consider it a step into the future. This project is a huge challenge: not only for us in terms of organization, but also for our partners – including Hicron – in terms of adapting the system to the needs and business models of PSA. Cooperation with Hicron consultants, taking into account their competences in the field of programming and processes specific to the automotive sector, gave us many reasons to be satisfied.