InsurTech Innovations: Transforming the Insurance Industry

- November 14

- 8 min

Marine insurance operates in one of the most complex and volatile risk environments in the global economy. With vessels traversing unpredictable waters, cargo exposed to numerous perils, and port operations facing constant operational challenges, the marine insurance sector requires sophisticated premium modeling approaches that can accurately price risk while maintaining profitability. The foundation of effective premium setting lies in the systematic analysis of claims history, which provides insurers with crucial insights into loss patterns, risk concentrations, and emerging threats.

The marine insurance market handles approximately $50 billion in annual premiums globally, covering everything from small coastal vessels to massive container ships worth hundreds of millions of dollars. This diverse portfolio requires nuanced underwriting approaches that can differentiate between various risk profiles while maintaining competitive pricing structures that attract quality business.

Key takeaways:

Claims history serves as the cornerstone of effective marine insurance pricing, providing empirical evidence of how risks materialize in real-world conditions. Unlike theoretical risk models, claims data reveals the actual frequency and severity of losses across different vessel types, trade routes, and operational scenarios. This historical perspective enables underwriters to identify patterns that might not be apparent through traditional risk assessment methods.

The importance of analyzing claims history extends beyond simple loss counting. Modern marine insurers examine claims data to understand

For instance, the introduction of advanced navigation systems has significantly reduced collision claims over the past decade, while climate change has increased the frequency of weather-related incidents in previously stable regions.

Accurate premium setting requires a deep understanding of how different factors influence claims outcomes. Claims history analysis reveals correlations between:

These insights enable insurers to develop more sophisticated pricing models that reflect actual risk exposure rather than relying solely on theoretical assessments.

These metrics directly impact cash flow projections and reserve requirements, making them essential components of premium calculations.

The integration of advanced analytics into marine insurance holds a promise for how insurers approach premium modeling and risk assessment.

|

Aspect |

Details |

|

Role of Machine Learning |

Machine learning processes vast data like claims histories, weather reports, and vessel tracking to uncover hidden risk patterns for more precise pricing. |

|

Data-Driven Underwriting |

Transforms underwriting into an evidence-based process by correlating numerous variables such as port congestion and seasonal trends with damage claims. |

|

Portfolio Management |

Advanced analytics model the cumulative impact of risks, revealing indirect exposures and risk concentrations across various policies. |

|

Dynamic Pricing Models |

Enables real-time adjustments to premium rates, adapting to changing risk conditions and improving accuracy over traditional actuarial methods. |

|

Reinsurance Integration |

Supports sustainable premium models by providing stability and capacity for catastrophic risks through advanced structures like parametric triggers and aggregate covers. |

Machine learning algorithms can now process vast amounts of claims data, weather information, vessel tracking data, and economic indicators to identify previously undetectable risk patterns. These analytical capabilities enable insurers to move beyond traditional actuarial methods toward dynamic pricing models that can adapt to changing risk conditions in real-time.

Data-driven strategies have transformed underwriting from a largely subjective process to an objective, evidence-based discipline.

Boston Consulting Group states that AI has improved efficiency in complex underwriting processes by up to 36%, with a 3% improvement in loss ratios through better data utilization.

Modern analytics can simultaneously correlate hundreds of variables, identifying subtle relationships between factors such as port congestion levels and cargo damage claims, or seasonal weather patterns and hull damage incidents. This comprehensive approach enables more accurate risk segmentation and pricing precision.

The influence of big data extends to portfolio management, where insurers can now model the cumulative impact of individual risks on overall portfolio performance. Advanced analytics help identify risk concentrations that might not be apparent through traditional underwriting methods, such as indirect exposures through supply chain dependencies or correlated risks across seemingly unrelated policies.

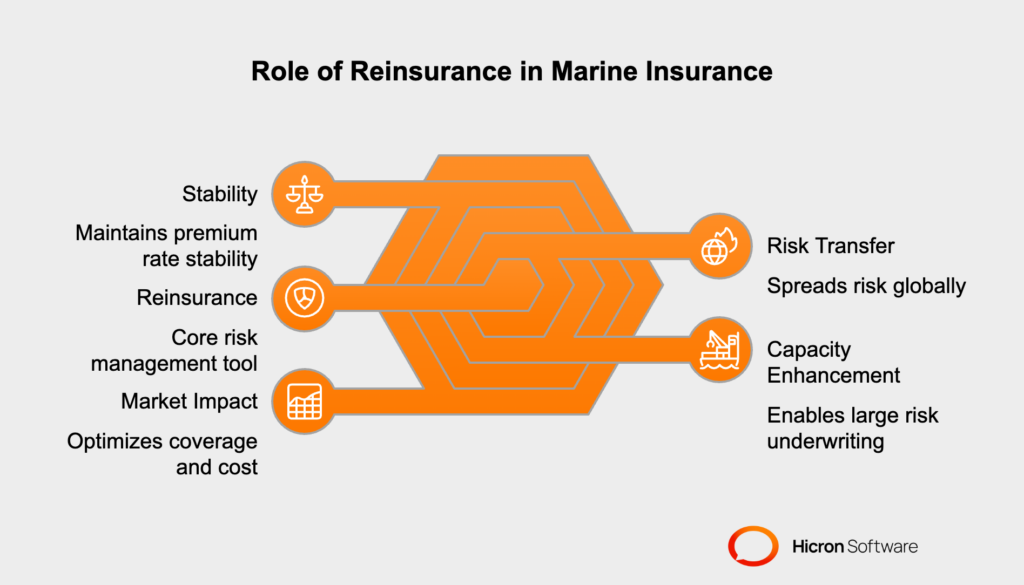

Reinsurance plays a crucial role in sustainable premium models by providing capacity for catastrophic losses and enabling insurers to write larger risks while maintaining capital efficiency. Modern reinsurance structures are increasingly sophisticated, incorporating parametric triggers, aggregate covers, and multi-year agreements that provide stability in volatile markets. The integration of reinsurance considerations into primary pricing models ensures that premium rates reflect the true cost of risk transfer while maintaining competitive positioning.

Loss ratios represent the fundamental measure of underwriting profitability in marine insurance, calculated as the ratio of incurred losses plus loss adjustment expenses to earned premiums. A loss ratio of 100% indicates that claims costs exactly equal premium income, while ratios above this threshold suggest underwriting losses. However, the interpretation of loss ratios in marine insurance requires careful consideration of the long-tail nature of many claims and the volatility inherent in marine risks.

Understanding loss ratios goes beyond simple calculation to encompass trend analysis, peer comparisons, and forward-looking projections. Marine insurers typically target combined ratios (loss ratio plus expense ratio) between 95% and 105%, allowing for investment income to generate overall profitability. Yet, this target can vary wildly based on market conditions, competitive pressures, and the specific risk profile of the portfolio.

Loss ratios serve as early warning indicators of portfolio deterioration, enabling insurers to implement corrective measures before losses become unsustainable. A gradual increase in loss ratios might indicate inadequate premium rates, deteriorating risk selection, or emerging perils that weren’t adequately priced. Conversely, consistently low loss ratios might suggest overly conservative pricing that could result in market share erosion.

Example: Consider a marine insurer writing cargo insurance with a historical loss ratio of 65%. If the loss ratio suddenly increases to 85% over two consecutive quarters, this could indicate several potential issues: inadequate rate increases to keep pace with inflation, deterioration in cargo handling standards at key ports, or increased theft and piracy in major trade routes. The insurer would need to investigate these factors systematically to determine whether premium adjustments, coverage modifications, or enhanced risk management requirements are necessary.

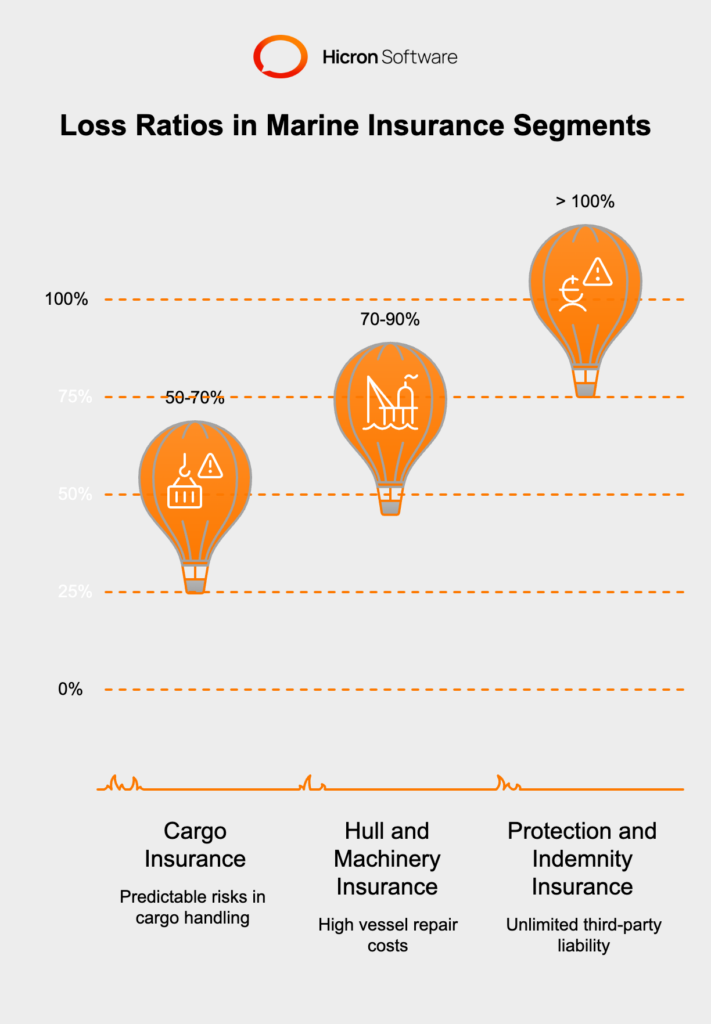

Marine insurance encompasses several distinct segments, each with unique risk characteristics and loss patterns. Cargo insurance typically exhibits loss ratios between 50-70%, reflecting the relatively predictable nature of cargo handling and transportation risks. However, this segment can experience significant volatility during periods of economic disruption, supply chain congestion, or extreme weather events.

Hull and machinery insurance generally shows higher loss ratios, often ranging from 70-90%, due to the complexity and high value of vessel repairs. The introduction of more sophisticated vessels with advanced technology has created a dichotomy in this segment, with newer vessels showing lower loss ratios due to improved safety systems, while older vessels experience increasing maintenance-related claims.

Protection and indemnity (P&I) insurance exhibits the most volatile loss ratios, sometimes exceeding 100% in years with major incidents. This volatility stems from the unlimited nature of third-party liability exposures and the potential for catastrophic environmental claims. The long-tail development of P&I claims also makes loss ratio analysis more challenging, as initial estimates may prove inadequate years after the incident occurs.

Example: The implementation of the International Maritime Organization’s sulfur emission regulations (IMO 2020) created a distinct trend in loss ratios across different segments. Cargo insurers initially saw increased claims related to fuel contamination and vessel delays as the industry adapted to new fuel specifications. Hull insurers experienced higher machinery claims as older engines struggled with low-sulfur fuels. However, P&I insurers benefited from reduced environmental claims as cleaner fuels decreased pollution incidents.

Risk selection represents the most direct method for optimizing loss ratios. It requires insurers to develop sophisticated screening processes that identify and attract low-risk exposures while avoiding or pricing adequately for high-risk scenarios. Effective risk selection combines traditional underwriting expertise with advanced predictive modeling capabilities to create a comprehensive assessment framework.

Predictive modeling has revolutionized risk selection by enabling insurers to quantify the probability of claims based on multiple risk factors simultaneously. These models incorporate vessel characteristics, operational patterns, crew qualifications, cargo types, trade routes, and historical performance to generate risk scores that guide underwriting decisions. The continuous refinement of these models based on actual claims experience ensures their accuracy and relevance.

Data quality in risk selection is crucial and cannot be overstated. Modern marine insurers invest heavily in data collection and verification processes, utilizing vessel tracking systems, port records, survey reports, and third-party databases to build comprehensive risk profiles. This information enables more accurate risk assessment and supports premium differentiation based on actual exposure levels.

Example: A marine insurer implemented a predictive model that incorporated vessel age, maintenance records, crew certification levels, and route characteristics to score cargo insurance risks. The model identified that vessels operating on certain trade routes with crews certified to international standards showed 30% lower claims frequency than the portfolio average. By adjusting premium rates to reflect this difference and actively marketing to operators meeting these criteria, the insurer improved their cargo portfolio loss ratio from 68% to 58% over two years while maintaining premium volume.

Claim frequency analysis provides crucial insights into the operational aspects of marine risks and helps insurers understand the underlying drivers of loss occurrence. High-frequency, low-severity claims often indicate systemic issues in cargo handling, vessel maintenance, or operational procedures, while low-frequency patterns might suggest effective risk management or potential exposure to severe but infrequent losses.

The impact of frequent small claims extends beyond their individual cost to affect the overall efficiency of the claims handling process and customer satisfaction. Marine cargo insurance, in particular, often deals with numerous small claims for minor cargo damage, container seal breaches, or documentation discrepancies. While individually insignificant, these claims can consume substantial administrative resources and indicate broader quality control issues in the supply chain.

Frequency analysis also reveals important trends related to technological advancement and industry practices. The widespread adoption of container tracking systems has reduced claims frequency related to cargo loss and theft, while improved weather forecasting has decreased weather-related incidents. However, the increasing complexity of modern vessels has introduced new types of frequent claims related to electronic system failures and cyber-related incidents.

Example: A marine cargo insurer noticed an increasing frequency of claims for electronic goods damaged during container handling at a major Asian port. Investigation revealed that new automated handling equipment was generating electromagnetic interference that affected sensitive electronic cargo. By working with the port authority to implement shielding solutions and adjusting coverage terms to exclude this specific peril until remediation was complete, the insurer reduced claim frequency by 40% while maintaining customer relationships.

Claim severity analysis focuses on understanding the potential magnitude of losses and the factors that influence the cost of individual claims. Marine insurance is particularly susceptible to severe losses due to the high values involved and the potential for catastrophic incidents affecting multiple parties. Effective severity analysis helps insurers establish appropriate policy limits, reinsurance structures, and reserve levels.

The importance of analyzing high-cost claims extends to understanding the effectiveness of loss mitigation measures and the impact of external factors on claim costs. Catastrophic cargo damage often results from cascading failures where initial incidents trigger secondary losses, such as refrigeration failures leading to cargo spoilage or fire incidents causing extensive contamination damage.

Historical analysis of severe claims provides valuable insights into loss development patterns and the factors that influence final settlement amounts. This analysis is particularly important for long-tail exposures where initial reserves may prove inadequate as the full extent of damages becomes apparent over time.

Example: The 2021 Ever Given Suez Canal blockage created a natural experiment in claim severity analysis. While the initial incident appeared to be a single vessel grounding, the resulting supply chain disruption generated thousands of claims across multiple insurance lines. Cargo insurers faced claims for delayed delivery, spoiled perishables, and manufacturing interruptions. The incident demonstrated how a single event could generate severe losses across seemingly unrelated policies, leading insurers to reassess their accumulation management and correlation modeling approaches.

Effective premium setting requires a sophisticated understanding of the relationship between claim frequency and severity, as these factors often exhibit inverse relationships that complicate pricing decisions. High-frequency, low-severity exposures require different pricing approaches than low-frequency, high-severity risks, and many marine risks exhibit characteristics of both patterns simultaneously.

The challenge in balancing these factors lies in developing pricing models that adequately account for both dimensions while remaining competitive in the marketplace. Insurers must consider the total cost of risk, including

while also factoring in the time value of money and investment income potential.

Practical strategies for managing this balance include developing differentiated pricing models that segment risks based on their frequency-severity profiles. High-frequency risks might warrant higher deductibles or co-insurance arrangements to align incentives for loss prevention, while high-severity risks might require specific coverage limits or exclusions to manage catastrophic exposure.

Practical Strategy: A marine insurer developed a tiered pricing structure for container cargo risks based on frequency-severity analysis. Low-value, high-frequency cargo (such as textiles) was priced with higher base rates but lower severity loadings, while high-value, low-frequency cargo (such as machinery) received lower base rates but higher severity charges. This approach better matched premium charges to actual risk costs and improved overall portfolio profitability by 15%.

Reinsurance serves as the backbone of marine insurance capacity, enabling primary insurers to write risks that would otherwise exceed their financial capabilities or risk tolerance. The role of reinsurance extends beyond simple risk transfer to include technical expertise, claims handling support, and market intelligence that enhances overall underwriting capabilities.

The critical nature of reinsurance in marine insurance stems from the potential for catastrophic losses that could threaten the solvency of primary insurers. Major maritime casualties can generate claims in the hundreds of millions or even billions of dollars, far exceeding the capacity of individual insurers. Reinsurance arrangements allow these risks to be spread across the global insurance market, ensuring adequate capacity for large risks while maintaining stability in premium rates.

Reinsurance structures in marine insurance have evolved to address specific risk characteristics and market needs. Proportional reinsurance provides capacity and spread risk across multiple carriers, while non-proportional reinsurance protects against severity through excess of loss covers. Modern reinsurance programs often combine multiple structures to optimize coverage and cost efficiency.

Example: Following a major container ship fire that generated $200 million in cargo claims, a primary marine insurer’s reinsurance program responded across multiple layers. The first $10 million was retained, with quota share reinsurers covering 50% of this retention. An excess of loss treaty covered the next $40 million, with a second layer covering an additional $100 million. This structure limited the primary insurer’s net retention to $5 million while providing full coverage for the loss, demonstrating the critical role of well-structured reinsurance in maintaining financial stability.

Reinsurance pricing directly reflects the claims experience of the underlying portfolio, creating a direct link between primary claims history and reinsurance costs. Reinsurers analyze claims data with even greater scrutiny than primary insurers, as they typically have less direct control over risk selection and claims handling processes.

The relationship between claims history and reinsurance pricing operates on multiple levels. Individual account experience affects specific treaty pricing, while broader market experience influences overall reinsurance market capacity and pricing trends. Reinsurers also consider the quality of the primary insurer’s underwriting and claims handling capabilities when setting prices, recognizing that these factors significantly influence ultimate loss outcomes.

Claims frequency and severity patterns have different impacts on reinsurance pricing structures. High-frequency patterns primarily affect proportional reinsurance costs, as these arrangements participate in all losses regardless of size. Severe loss patterns have greater impact on excess of loss pricing, where reinsurers focus on the potential for large individual losses or accumulations.

Example: A marine insurer experienced a deteriorating loss ratio in their hull portfolio, increasing from 75% to 95% over three years due to an aging fleet and deferred maintenance issues. When their proportional reinsurance treaty came up for renewal, reinsurers increased the commission by 5 percentage points and implemented additional underwriting guidelines requiring pre-renewal surveys for vessels over 15 years old. The insurer was forced to either absorb the additional cost or pass it through to policyholders via premium increases, demonstrating the direct impact of claims experience on reinsurance costs.

Reinsurance enables marine insurers to participate in high-risk, high-reward segments that would otherwise be unavailable due to capital constraints or risk tolerance limitations. Strategic use of reinsurance allows insurers to maintain diversified portfolios while managing concentration risk and protecting their capital base.

The management of high-risk marine policies through reinsurance requires careful consideration of coverage structures, retention levels, and reinsurer selection. Different types of high-risk exposures may require different reinsurance approaches, from specific risk excess covers for individual large vessels to aggregate covers for exposure concentrations in particular geographical areas or industry segments.

Structured reinsurance partnerships have become increasingly important in managing complex marine risks, with reinsurers providing not just capacity but also technical expertise and risk management support. These partnerships often involve multi-year agreements that provide stability and encourage long-term relationship building between primary insurers and reinsurers.

Example: A specialty marine insurer wanted to participate in the offshore energy market but lacked the technical expertise and capital capacity to write these risks directly. They established a partnership with a leading marine reinsurer that provided 75% quota share capacity along with technical underwriting support and claims expertise. This arrangement allowed the primary insurer to build expertise gradually while the reinsurer gained access to a new distribution channel, creating a mutually beneficial relationship that enabled both parties to expand their market presence.

Artificial intelligence and machine learning have transformed marine insurance pricing by enabling the analysis of complex, multi-dimensional datasets that would be impossible to process using traditional methods. These technologies can identify subtle patterns and relationships in claims data that human underwriters might miss, leading to more accurate risk assessment and pricing precision.

The enhancement of claims analysis through AI extends beyond simple pattern recognition to include predictive capabilities that forecast future claim frequencies and severities based on changing risk factors. Machine learning algorithms can continuously update their predictions as new data becomes available, ensuring that pricing models remain current and accurate.

Modern predictive models incorporate diverse data sources including weather patterns, economic indicators, vessel tracking information, and real-time operational data to create comprehensive risk assessments. This holistic approach provides a more complete picture of risk exposure and enables more nuanced pricing decisions.

Example: A marine insurer implemented a machine learning model that analyzed vessel movement patterns, port congestion data, weather forecasts, and historical claims data to predict cargo damage probability for specific voyages. The model identified that vessels spending more than 48 hours in port during peak congestion periods showed 25% higher damage rates due to rushed handling. This insight enabled the insurer to offer dynamic pricing based on planned port call durations, improving risk selection while providing customers with incentives for better voyage planning.

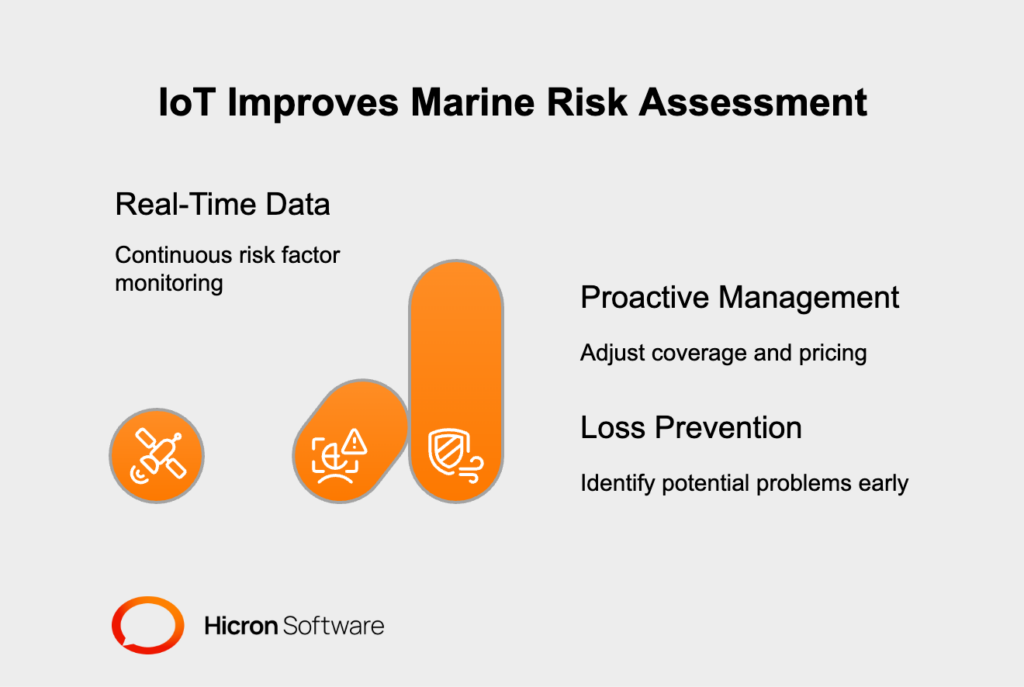

The Internet of Things (IoT) and telematics have revolutionized marine risk assessment by providing real-time visibility into vessel operations, cargo conditions, and environmental factors. This technology enables proactive risk management and more accurate pricing based on actual operational performance rather than historical averages.

Real-time data integration allows insurers to monitor risk factors continuously and adjust coverage or pricing as conditions change. Vessel tracking systems provide information on route deviations, speed variations, and port call patterns that can indicate increased risk exposure. Similarly, cargo monitoring systems can detect temperature variations, humidity changes, or shock events that might lead to cargo damage claims.

The importance of IoT and telematics extends to loss prevention, where real-time monitoring can identify potential problems before they result in claims. Early warning systems can alert crews to mechanical issues, weather hazards, or security threats, enabling preventive actions that reduce both claim frequency and severity.

Example: A marine insurer partnered with a telematics provider to monitor refrigerated cargo containers in real-time. The system tracked temperature, humidity, and door openings throughout the supply chain journey. When temperature excursions were detected, automatic alerts were sent to cargo handlers and the insurer’s claims team. This proactive approach reduced refrigerated cargo claims by 35% while improving customer satisfaction through better cargo protection. The insurer also used the data to offer premium discounts to shippers who maintained consistent temperature control throughout their supply chains.

Automated systems have transformed claims processing in marine insurance by enabling faster, more accurate handling of routine claims while freeing human adjusters to focus on complex or high-value losses. The role of automation extends from initial claim reporting through final settlement, streamlining processes that traditionally required significant manual intervention.

The handling of high claim volumes through automation is particularly important in marine cargo insurance, where thousands of small claims must be processed efficiently to maintain customer satisfaction and control administrative costs. Automated systems can verify policy coverage, assess liability, and calculate settlements for straightforward claims without human intervention.

AI tools are increasingly sophisticated in their ability to analyze claim documentation, identify fraud indicators, and recommend appropriate reserve levels. These capabilities improve both the speed and accuracy of claims processing while reducing the potential for human error or bias in claim evaluation.

Example: A marine insurer implemented an AI-powered claims processing system for cargo damage claims under $10,000. The system could automatically verify policy coverage, analyze shipping documents, assess damage photos, and calculate settlements within minutes of claim submission. For straightforward claims meeting specific criteria, payments were authorized and issued automatically. This automation reduced average processing time from 15 days to 2 days while maintaining accuracy levels above 95%, significantly improving customer satisfaction and reducing administrative costs.

Building and maintaining comprehensive claims databases represents a critical investment in the analytical capabilities that drive effective premium modeling. These databases must capture both basic claim information and detailed risk factors, loss circumstances, and resolution outcomes, enabling sophisticated analysis and modeling.

The aggregation of data for loss ratio and trend analysis requires careful consideration of data structure, quality controls, and analytical requirements. Modern claims databases incorporate structured and unstructured data, including claim adjuster reports, survey findings, legal documents, and external data sources such as weather records and economic indicators.

Effective claims databases enable segmentation and analysis across multiple dimensions, allowing insurers to identify trends by geography, vessel type, cargo category, time period, and numerous other factors. This granular analysis capability supports more precise pricing and risk selection decisions.

Example: A global marine insurer developed a comprehensive claims dashboard that segmented data by region, policy type, and claim type, enabling real-time monitoring of portfolio performance. The system integrated data from multiple subsidiaries and provided standardized reporting that facilitated comparison across different markets. Regional managers could identify emerging trends in their territories, while corporate underwriters could adjust global pricing guidelines based on aggregated experience. This capability enabled the insurer to respond more quickly to changing risk conditions and maintain competitive pricing while protecting profitability.

The importance of partnerships between primary insurers and reinsurers extends beyond simple risk transfer to encompass shared expertise, joint risk assessment, and collaborative loss prevention initiatives. These partnerships enable more comprehensive risk management approaches that benefit all parties involved.

Modern reinsurance relationships involve joint risk assessment initiatives where reinsurers contribute their global experience and technical expertise to help primary insurers evaluate complex risks. This collaboration is particularly valuable in emerging risk areas where individual insurers may lack sufficient experience to make informed underwriting decisions.

The sharing of claims data and analysis between primary insurers and reinsurers creates opportunities for enhanced risk understanding and improved loss prevention. Reinsurers often have broader market perspectives that can identify emerging trends or risk concentrations that individual primary insurers might miss.

Example: A marine insurer partnered with their reinsurers to conduct joint risk assessments for offshore wind farm construction projects. The reinsurers provided technical expertise on foundation installation risks and weather-related exposures, while the primary insurer contributed knowledge of local conditions and contractor capabilities. This collaboration enabled more accurate pricing and risk management recommendations, resulting in profitable participation in a growing market segment while maintaining appropriate risk controls.

The use of claims experience to adjust and refine premium structures represents an ongoing process that requires systematic analysis and regular model updates. Continuous feedback loops ensure that pricing models remain accurate and responsive to changing risk conditions while maintaining competitive positioning.

Premium model refinement involves analyzing variances between expected and actual claims experience, identifying the factors that contributed to these variances, and adjusting model parameters accordingly. This process requires sophisticated analytical capabilities and strong feedback mechanisms between underwriting, actuarial, and claims functions.

The implementation of continuous feedback systems enables more dynamic pricing approaches that can respond quickly to emerging trends or changing risk conditions. Regular model updates ensure that pricing remains aligned with actual risk costs while maintaining the stability needed for effective business planning.

Example: A marine insurer implemented quarterly premium model reviews that analyzed claims experience by major risk categories and adjusted pricing parameters based on emerging trends. When analysis revealed that cyber-related claims were increasing faster than anticipated, the insurer quickly implemented enhanced screening procedures and adjusted pricing for vessels with sophisticated electronic systems. This proactive approach enabled the insurer to maintain profitability while competitors struggled with unexpected losses in this emerging risk area.

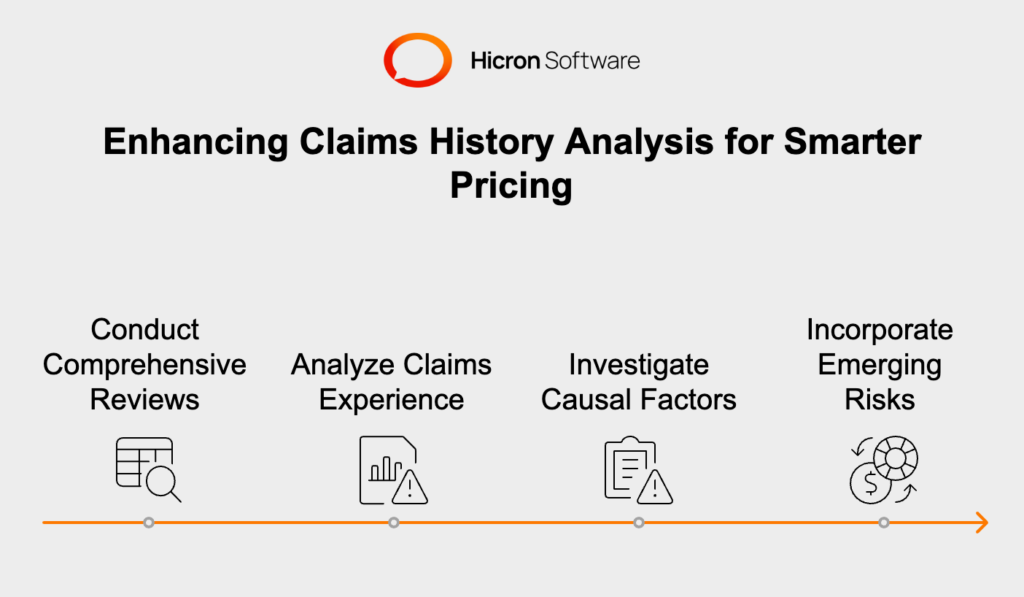

Conducting comprehensive reviews of existing claim data represents the foundation of effective premium optimization, requiring systematic analysis of historical experience combined with forward-looking assessment of emerging risks. This process must be thorough, objective, and focused on actionable insights that can improve pricing accuracy and risk selection.

The review process should encompass all aspects of claims experience, including frequency patterns, severity trends, loss development characteristics, and claim closure rates. Analysis should extend beyond simple statistical summaries to include investigation of underlying causal factors and identification of potential prevention opportunities.

Emerging risks present particular challenges for claims history analysis, as historical data may not provide adequate guidance for future pricing. Insurers must develop approaches for incorporating new risk factors and adjusting pricing models based on limited experience and expert judgment.

Example: A marine insurer conducted a comprehensive review of their container cargo claims over a five-year period, analyzing patterns by trade route, cargo type, season, and handling location. The analysis revealed that claims rates were 40% higher during peak shipping seasons due to rushed handling and port congestion. Additionally, certain trade routes showed increasing theft rates that weren’t reflected in current pricing. Based on these insights, the insurer implemented seasonal pricing adjustments and enhanced security requirements for high-risk routes, resulting in improved loss ratios and better risk selection.

The incorporation of reinsurance considerations into initial pricing models ensures that premium rates reflect the total cost of risk transfer while maintaining competitive positioning. This integration requires careful analysis of reinsurance costs, terms, and availability across different risk categories and market conditions.

Building resilient premium models requires consideration of various reinsurance structures and their cost implications. Proportional reinsurance affects pricing differently than excess of loss coverage, and the choice of structure can significantly impact the economics of different risk categories.

Pre-negotiated terms with reinsurers provide stability and predictability in pricing while enabling insurers to respond quickly to market opportunities. These arrangements require careful planning and strong reinsurer relationships built on mutual trust and shared risk understanding.

Example: A marine insurer negotiated a multi-year reinsurance facility with pre-agreed terms for high-value cargo risks, providing capacity up to $100 million per risk with fixed pricing for risks meeting specified criteria. This arrangement enabled the insurer to quote large cargo risks immediately without waiting for reinsurer approval, improving their competitive position while maintaining cost predictability. The pre-negotiated terms also included provisions for capacity increases based on business volume, supporting the insurer’s growth objectives in this market segment.

The evolution of marine insurance pricing continues to accelerate with advances in data analytics, artificial intelligence, and real-time monitoring technologies. Future premium models will likely incorporate even more sophisticated predictive capabilities, dynamic pricing mechanisms, and automated decision-making processes that can respond to changing risk conditions in real-time.

Claims history will remain central to these developments, but the analysis will become more sophisticated and comprehensive. Integration of external data sources, predictive modeling, and scenario analysis will enable more accurate pricing and better risk selection while maintaining the flexibility needed to adapt to changing market conditions.

The summary of how claims history shapes effective pricing strategies emphasizes the critical importance of systematic data collection, rigorous analysis, and continuous model refinement. Success in this environment requires investment in analytical capabilities, technology infrastructure, and human expertise that can translate complex data into actionable underwriting and pricing decisions.

Leveraging technology and reinsurance for adaptive premium models represents the path forward for marine insurers seeking to maintain profitability while providing competitive coverage for their customers. This approach requires strong partnerships, sophisticated analytical capabilities, and the flexibility to adapt quickly to changing market conditions and emerging risks.

The vision of a resilient marine insurance market driven by claims insights and innovation represents an achievable goal that requires commitment, investment, and collaboration across the industry. This future market will be characterized by more accurate pricing, better risk selection, and enhanced loss prevention capabilities that benefit all stakeholders.

Creating sustainable solutions requires a long-term perspective that balances profitability with market stability and customer needs. Claims-informed pricing must be implemented in ways that encourage risk improvement and loss prevention rather than simply penalizing poor experience. This approach creates positive feedback loops that benefit the entire marine transportation industry.

The call to action for insurers to prioritize continuous improvements in claims-based pricing reflects the competitive necessity of analytical excellence in modern insurance markets. Insurers that fail to invest in these capabilities will find themselves at a disadvantage in both pricing accuracy and risk selection, ultimately affecting their market position and profitability.

Success in this environment requires commitment to data quality, analytical rigor, and continuous improvement. Insurers must view claims history analysis not as a periodic exercise but as an ongoing competitive advantage that drives better decision-making across all aspects of their business operations.

The marine insurance premium is the amount paid by the insured to the insurer in exchange for coverage against risks related to maritime activities, such as cargo shipment, vessel operations, or transport by sea, air, or land.

An insurance premium is the cost paid by a policyholder to an insurance company for coverage over a specified period. It is determined based on factors like risk level, coverage type, and policy terms.

Marine insurance is a type of insurance that protects against damages or losses involving cargo, ships, terminals, and any transport vehicles involved in moving goods by sea or other transit routes.

A 10% markup is often added to the insured value to cover incidental or unforeseen charges like freight costs or handling fees, ensuring full compensation in case of loss.

The three main types of marine insurance are:

Cargo Insurance: Covers goods transported by ships or other modes during transit.

Hull Insurance: Protects the vessel and its equipment.

Liability Insurance: Covers legal liabilities arising from damages caused by the vessel to third parties.

The cost of marine insurance varies depending on factors such as the value of the goods, type of cargo, shipping route, and level of coverage. Premiums are typically expressed as a percentage of the total value insured.

In general, insurance premiums are calculated using the formula:

Premium = Sum Insured × Rate of Premium ÷ 100

The rate of premium may depend on risks, coverage type, and policy terms.

A premium type of insurance refers to the category or pricing structure for coverage. It indicates whether the policy is standard, high-risk, or specialized, influencing the premium amount charged based on associated risks.

Claims history provides empirical data on past losses, including frequency and severity trends. It helps insurers understand risk patterns, such as seasonal variations, geographical concentrations, and the impact of vessel age or cargo type, which are crucial for setting accurate and competitive premiums.

Advanced analytics, including machine learning, processes large datasets to uncover hidden risk patterns. Incorporating variables like port congestion, vessel tracking, and weather forecasts enables dynamic pricing models that adapt to changing risk conditions in real time.

Reinsurance mitigates financial risks associated with catastrophic losses, enabling primary insurers to maintain stable premium rates while taking on high-value or volatile risks. Sophisticated reinsurance structures, such as parametric triggers or aggregate covers, ensure resilience and underwriting capacity.

Insurers use tailored pricing strategies to account for both claim frequency and severity. For example, high-frequency risks may involve higher deductibles, while catastrophic loss scenarios require specific policy limits, enhanced reinsurance coverage, or exclusions for effective risk management.

Real-time data from IoT and telematics enhances risk assessment by monitoring vessel operations, cargo conditions, and environmental factors. This proactive visibility reduces claim frequency, aids loss prevention, and supports dynamic premium adjustments, benefiting both insurers and clients.

The basic formula for calculating a marine insurance premium is:

Marine Insurance Premium = Insured Value × Rate of Premium

Where:

Insured Value: The total value of the goods or property being insured, including the cost of the goods, freight charges, and any additional expenses (often referred to as CIF value: Cost + Insurance + Freight).

Rate of Premium: The percentage rate determined by the insurer based on factors like the type of cargo, route, mode of transport, and risk level.

For example, if the insured value of goods is $100,000 and the premium rate is 0.5%, the premium would be:

$100,000 × 0.005 = $500

Additional charges or discounts may apply based on specific policy terms or risk factors.

It automates claims validation by cross-referencing shipment data, incident reports, and policy terms in real time. With advanced features like document automation and fraud detection, it ensures faster processing and resolution of claims.

Hicron Software proved to be a trusted partner with unmatched technical expertise, delivering a scalable and user-friendly web application that was pivotal to our successful U.S. market expansion.

Hicron’s contributions have been vital in making our product ready for commercialization. Their commitment to excellence, innovative solutions, and flexible approach were key factors in our successful collaboration.

I wholeheartedly recommend Hicron to any organization seeking a strategic long-term partnership, reliable and skilled partner for their technological needs.

After carefully evaluating suppliers, we decided to try a new approach and start working with a near-shore software house. Cooperation with Hicron Software House was something different, and it turned out to be a great success that brought added value to our company.

With HICRON’s creative ideas and fresh perspective, we reached a new level of our core platform and achieved our business goals.

Many thanks for what you did so far; we are looking forward to more in future!

Hicron is a partner who has provided excellent software development services. Their talented software engineers have a strong focus on collaboration and quality. They have helped us in achieving our goals across our cloud platforms at a good pace, without compromising on the quality of our services. Our partnership is professional and solution-focused!

The IT system supporting the work of retail outlets is the foundation of our business. The ability to optimize and adapt it to the needs of all entities in the PSA Group is of strategic importance and we consider it a step into the future. This project is a huge challenge: not only for us in terms of organization, but also for our partners – including Hicron – in terms of adapting the system to the needs and business models of PSA. Cooperation with Hicron consultants, taking into account their competences in the field of programming and processes specific to the automotive sector, gave us many reasons to be satisfied.